We often hear of the importance of rebalancing, but how important is it really? The answer isn’t as simple as more frequent rebalancing is better; you must also consider the costs (turnover and trading costs). Instead we need to ask: when do the benefits of rebalancing outweigh the costs of implementation? What market conditions call for portfolio allocations to be managed more frequently? And under what conditions are the marginal costs greater than the benefits?

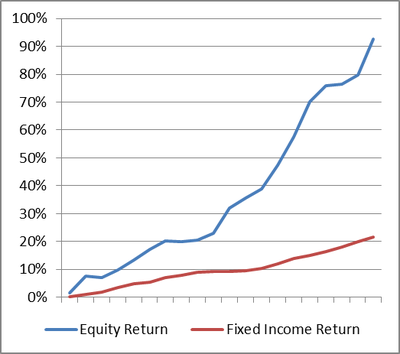

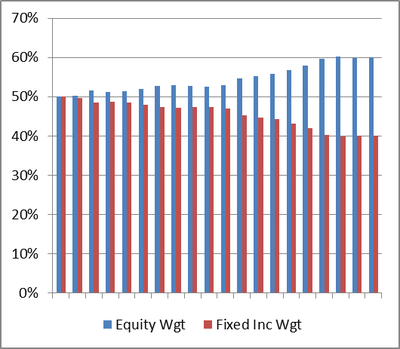

In general, a portfolio will have a higher return without rebalancing (buy-and-hold) during a trending upmarket. This concept is relatively simple. When one asset class (e.g., equities) is consistently outperforming, your weight will increase and thus capture more of the subsequent outperformance.

| Trending Market (Equity Outperforming) | Buy and Hold Weights in Trending Market |

|

|

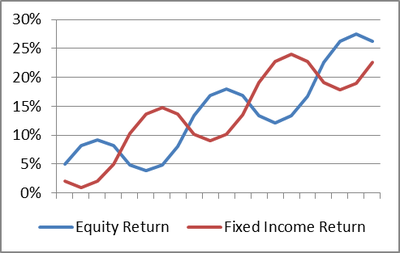

On the contrary, a portfolio will have a higher return with high frequency rebalancing during an oscillating market. By rebalancing during an oscillating market, additional funds are reallocated to sectors or asset classes whose weights have drifted lower but are set to outperform on the rebound.

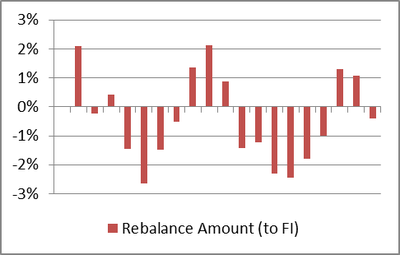

| Oscillating Market | Weight Shift for Rebalancing |

|

|

The concepts above are great if our only concern is total return and if we know exactly where the market is headed. However, some may argue that if we KNOW with certainty that equities will outperform fixed income, we should invest 100% in equity and 0% in fixed income and maximize return.

Because we don’t know the future with certainty, a big piece of any asset allocation strategy is hedging against that uncertainty. If a portfolio’s long-term strategy calls for a particular asset allocation split, then we should focus less on trying to time the market and more on the observable trends that may justify more frequent rebalancing. For example, take a strategy with a mandate of 75% equity/25% fixed income. How do we quantify the effect of rebalancing a 75/25 portfolio monthly vs. quarterly vs. annually?

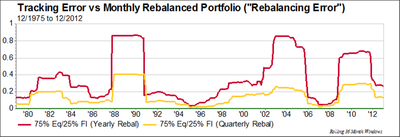

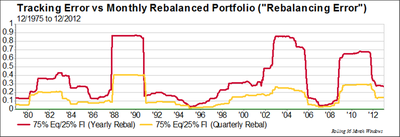

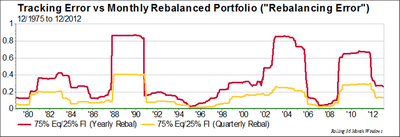

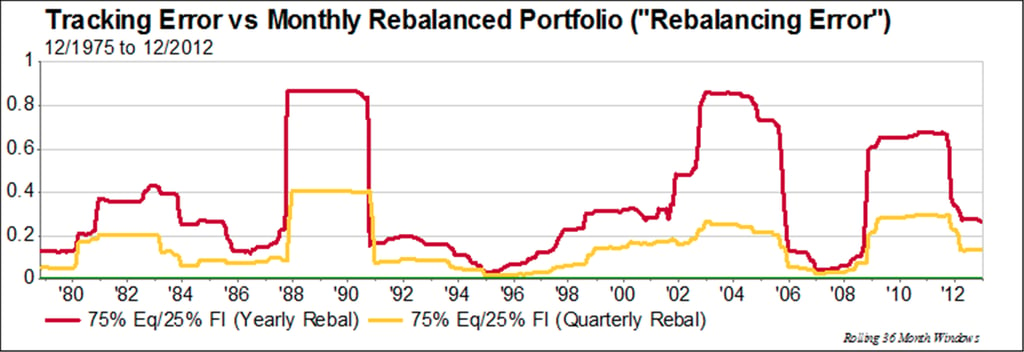

Since our portfolio objective specifies a 75/25 split, one measure of rebalancing risk is the tracking error of a yearly or quarterly rebalanced portfolio versus the constantly rebalanced 75/25 mandate (or “rebalancing error”):

Any spikes (high rebalancing error periods) indicate a stronger need for frequent rebalancing. Any dips or areas where the lines converge indicate there’s less benefit to rebalancing. For example, in 1989 rebalancing quarterly instead of yearly would have cut the rebalancing error by more than half (0.87 to 0.41). On the other hand, in 1995 the yearly rebalancing error decreased to 0.04, meaning that there was little difference attributed to the rebalance frequency and probably not enough benefit to justify any extra costs.

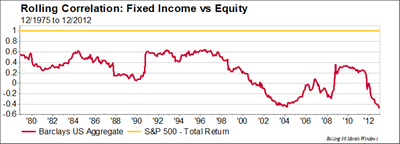

1. Correlation

In general, the differences in rebalancing error widen whenever correlation decreases. Uncorrelated asset classes lead to larger drifts in weight which left unaddressed lead to bigger differences in returns versus a rebalanced portfolio (e.g., higher rebalancing error).

2. Volatility

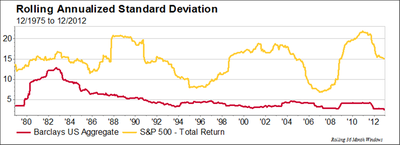

Fixed income volatility has steadily decreased, and we don’t see many large swings. A better gauge is equity volatility. In general, higher equity volatility appears to correlate to a higher rebalancing error (see 1989, 2003, and 2011) and lower volatility correlates to lower rebalancing error (1995, 2007).

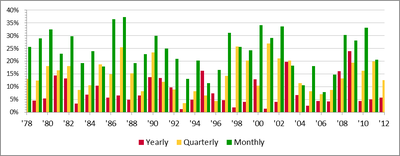

It is difficult to deduce a clear trend with the turnover chart above, but here are some general takeaways:

The volatility and correlations of asset classes should play a large role in determining whether or not more frequent rebalancing is needed. Recent market conditions are unlike any other period in recent history, with high volatility, extremely low correlations, and high domestic equity returns: four-year average equity returns close to 15%. The benefit of frequent rebalancing (i.e.,reducing rebalancing error) should be weighed against the cost (turnover and trading costs) to determine your own optimal rebalance policy and ensure that you’re prepared for future uncertainty in the market.

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

Stress Test Your Portfolio Using 1990 and 2003 Middle East Conflict Scenarios

Explore how to leverage two FactSet hypothetical scenarios based on historical Middle East conflicts and stress test your...

Geopolitical Risk Scenarios: Stress Testing Investment Strategies Amid the War in Iran

Stay ahead of evolving markets with a stress testing module from FactSet. Use it as your starting point and build in your...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)