On this stage, we have discussed the suitability of a risk model in terms of matching its forward looking horizon to a client’s investment process. I’m the first to agree that this indeed is an important dimension and should be considered carefully. What use has a risk prediction if the information is too late to react to? That said, I have noticed a trend among the different risk model providers to provide shorter term horizons in addition to their standard models. Both Barra and Axioma provide shorter and longer term versions of their risk models, and Northfield has produced near term versions of most of its models. The major focus of such models is to pick up increased levels of risks faster. Now, one could philosophise whether these additional horizons have arrived in time and whether they could have provided adequate warning signals for the multi sigma events we encountered in late 2008, but the fact remains that these models are here now and can provide useful insight if deployed in the right manner.

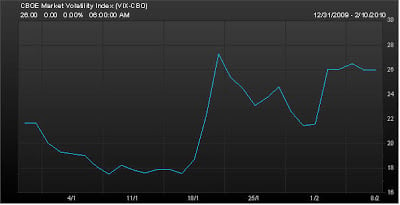

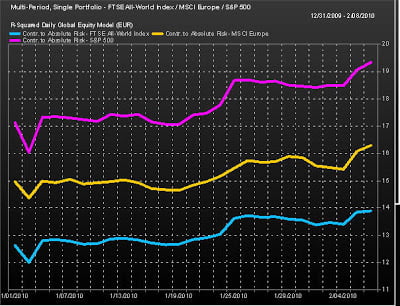

To highlight this responsiveness, consider the observed jump in the VIX over the last couple of weeks (while not all encompassing, the VIX is considered a valid proxy as a broad indication of perceived risk in the markets). As a broad indicator, the recent movement gives as an opportunity to see if and when a short-term model picks up on such an event. To do so, I decided to look at the absolute risk levels of some broad indices, in this case the FTSE All World, S&P 500, and MSCI Europe. I did this using the R-Squared Global Risk model, a daily updated model designed to predict risk on the ultra short horizon and to be very responsive.

Considering the above charts, we clearly see increases in the levels of risk after spikes in the VIX, especially during the last week. The magnitude of the impact in the spike seems related to the amount of exposure to the U.S. Market in our three indices (VIX is a measure of the volatility of the U.S. S&P 500 Index options).

Now consider the monitored impact on a monthly model. It’s going to be both less timely and a more drastic. This because the factor variances will be updated from month end to month end, so a fund may perceive a shock in predicted risk from one day to the other (when the model updates), while the fund composition itself didn’t change.

We’re not suggesting a quick fix here, saying one should only look at short term risk. But we do advocate multiple horizon measurement; longer term risk management may reflect the strategy of a fund, but when markets volatility rises, the information and analysis permitted through a shorter term model carries real value.

Total Portfolio Approach: The Plumbing Beneath the Philosophy

Explore this FactSet perspective on the total portfolio approach. Learn factors to consider if you want to effectively...

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)