In April, I presented on the topic of Geographic Revenue Exposures at the CFA Institute’s Annual Conference in Frankfurt, Germany. The inspiration for the talk stemmed from a request that I received from the portfolio manager of a U.S. large cap equity fund during my days as a FactSet Consultant 15 years ago. Well aware that a company’s risks and exposures are not solely determined by its country of domicile, my client explained that he wanted to aggregate the disparate geographic segment data reported by the companies held in his portfolio to better understand the portfolio’s overall exposure to countries and regions outside of the U.S.

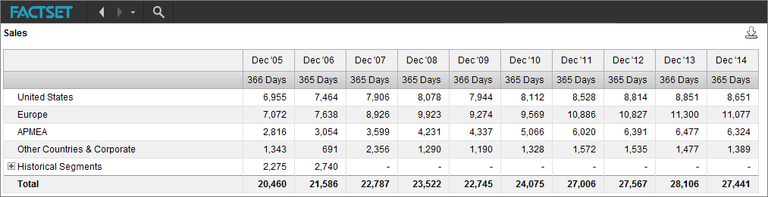

We can understand why my client made this request by examining McDonald’s latest annual filings, shown below, which illustrate both the usefulness and limitations of this information. This disclosure deconstructs McDonald’s revenue into four geographic regions, the U.S., Europe, APMEA, and Other Countries and Corporate, which can be used to help portfolio managers formulate ideas on how changes in those various regions might impact McDonald’s overall revenue. While this breakdown is somewhat useful, it presents two problems. First, the regional definitions are not standardized, which makes it very difficult to compare McDonald’s to other companies. Second, they’re extremely broad, making it challenging to examine the potential impact of events taking place in single countries. This lack of standardization and granularity, just as prevalent 15 years ago, meant that I was unable to provide an adequate solution for my client’s request at the time.

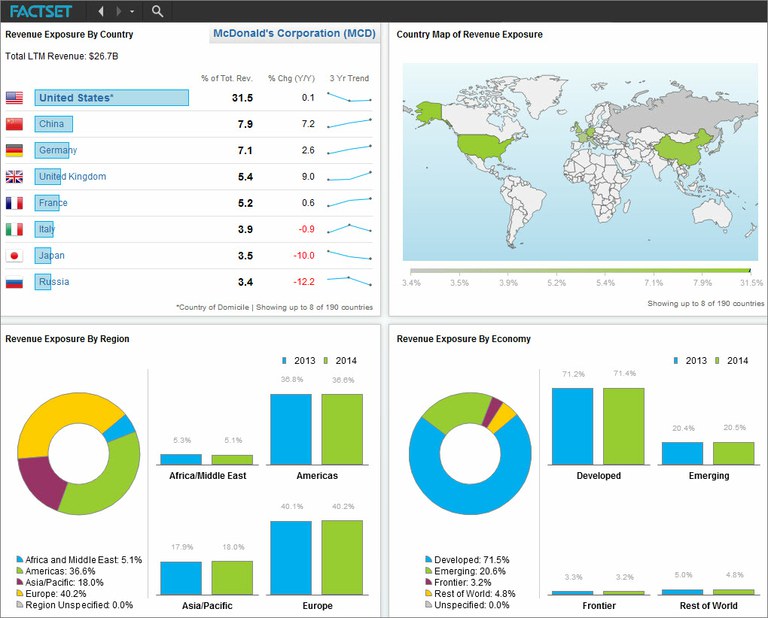

Today, using FactSet GeoRev data, we can correlate revenue to a normalized geographic classification system of nearly 300 countries, areas, regions, and super-regions, to make analysis across countries simple and efficient. Consider the revenue attribution for McDonald’s below.

Thanks to the normalization of the data, managers can now answer questions on an aggregate level. For example, it is now possible to examine the degree to which a developed market equity portfolio is exposed to emerging market economies, or seek out alpha by analyzing the link between a company’s exposure to countries where GDP is rising or falling, or where consumer sentiment is experiencing a sharp rise.

As my client realized all those years ago, country of domicile is no longer an accurate reflection of a company’s geographic exposure. I am already starting to see clients move from just examining individual companies to analyzing entire portfolios and benchmarks and adjusting their investment processes to incorporate this data. Knowing a portfolio’s true risk based on geographic revenue, with the standardization and granularity that has long been lacking, is able to provide investment professionals another vector of information for their disposal, and if you choose to ignore this additional vantage point you do so at your own peril!

Insight/Author%20Bios/Contributor_Photos/AndrewKovacs.jpg)

Mr. Andrew Kovacs is a Vice President and Senior Principal Product Manager at FactSet, based in the UK. In this role, he leads FactSet's development of off-platform workflow solutions in the areas of quant, risk, regulatory, and compliance. Prior to this role, Mr. Kovacs was Director of Quantitative Strategy for on-platform solutions. During his 20+ years at FactSet, he has also led Analytics specialist teams in APAC, EMEA, and the Americas. Mr. Kovacs earned a bachelor’s degree in finance and information systems from Boston College and is a CFA charterholder.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

Hyperscalers Tap External Financing as AI Capex Outruns Cash Flow

Explore this FactSet analysis of what is driving the funding shift among the five major hyperscalers plus implications for credit...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.