With U.S. stock indices in the red to start the year and market volatility beginning to climb, some are suggesting that investing in the defensive sectors may be a smart bet. The intuition here is that companies in the defensive sectors, like Consumer Staples, Utilities, and Health Care, have lower betas and are, therefore, less prone to changes in the business cycle. Do defensive sectors outperform in down markets and, if so, by how much? How do defensive sectors perform during varying levels of market volatility?

For this report’s analysis, the Consumer Staples, Utilities, and Health Care sectors are classified as the defensive sectors (“Defensives”), and the S&P Composite 1500 (“benchmark”) is used as the universe.

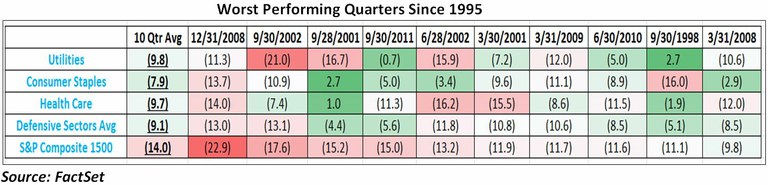

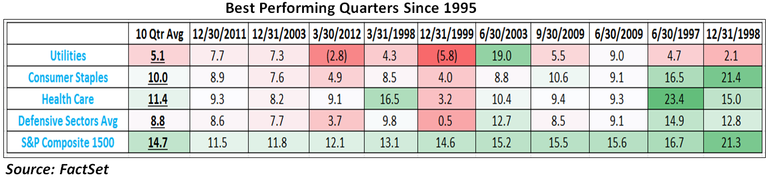

The top ten and bottom ten quarters since 1995, ranked by S&P Composite 1500 quarterly price returns, are shown in the table below. In the 10 worst performing quarters, the Defensives outperformed the benchmark in every quarter. On average, the performance of Defensives across those periods exceeded that of the S&P Composite 1500 by 4.9 percentage points. Defensives had a quarterly average return of -9.1%, while the benchmark had a return of -14%. In the 10 best performing quarters, the Defensives underperformed the benchmark in every quarter. On average, the performance of Defensives across those periods trailed that of the S&P Composite 1500 by 5.9 percentage points. Defensives had a quarterly average return of 8.8%, while the benchmark had a return of 14.7%.

Looking at price returns on a monthly basis from February 1995 through January 2016, the S&P Composite 1500 had been in the black for 155 months and in the red for 97 months (252 months total). Out of those down months, the Defensives outperformed the benchmark about 80% (78 out of 97 months) of the time and posted an average return that was 2.1 percentage points greater than the benchmark. Out of those up months, Defensives outperformed the S&P Composite 1500 about 33% (51 out of 155 months) of the time and saw an average return that was 1.3 percentage points lower than the benchmark.

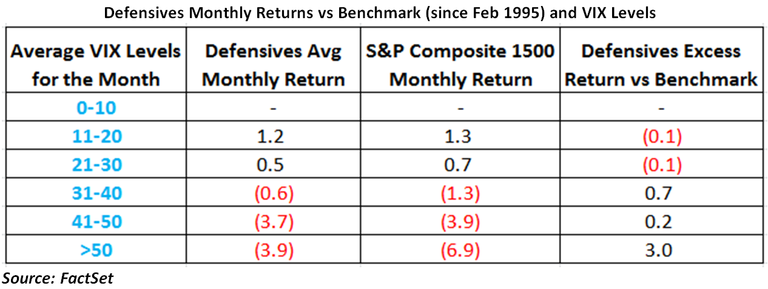

Using the CBOE Volatility Index (VIX) as a gauge of market volatility, the performance of Defensives has exceeded that of the benchmark at higher levels of volatility since 1995. For the months in which the average daily VIX levels surpassed 50, Defensives experienced an average monthly price return of -3.9%, while the S&P Composite 1500 saw a price return of -6.9%. This excess return of 3.0 percentage points represented the largest positive return over the benchmark out of all volatility buckets shown below (0-10, 11-20, 21-30, 31-40, 41-50, >50). Defensives outperformed the benchmark for the months in which average VIX levels were between 31 and 40 (+0.7 percentage points) and between 41 and 50 (+0.2 percentage points). However, they underperformed the benchmark at lower volatility levels as shown below. As of the close of the market on January 29, the VIX stood at 20.1, which was an 11% increase from its level at the end of 2015.

Since 1995, there have been two recessions in the United States. The first started on April 2, 2001 and ended on December 3, 2001 and the second started on January 2, 2008 and ended on July 1, 2009. During these periods, Defensives declined -14.4% on average, while the S&P Composite 1500 declined -18.1%. It is interesting to note that in the 2008-2009 financial crisis, the average VIX level throughout the crisis was 35. During this period, Defensives outperformed the benchmark by 11.3 percentage points. In the 2001 recession, the average VIX level was only 26. During this period, the S&P Composite 1500 actually outperformed Defensives by 3.9 percentage points. This is consistent with the data table above which shows that returns for Defensives don’t tend to exceed the benchmark until average volatility levels rise above 30.

U.S. ETF Monthly Summary: June 2025 Results

Get the latest monthly U.S. ETF flow results in this FactSet analysis. Learn flows by asset class and sector, ETF launches, and...

U.S. Mergers & Acquisitions Monthly Review: May 2025

Explore FactSet's U.S. Mergers & Acquisitions Monthly Review. Gain deep insights into market trends and expert analysis to inform...

Trading on Tariffs: Weighing Alternative Investments in an Uncertain International Trade Environment

Discover tariff impact on alternative investments and emerging markets, using Cobalt data to guide investor strategies amid...

U.S. ETF Monthly Summary: May 2025

U.S. ETF assets under management increased to $11.05 trillion in May.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.