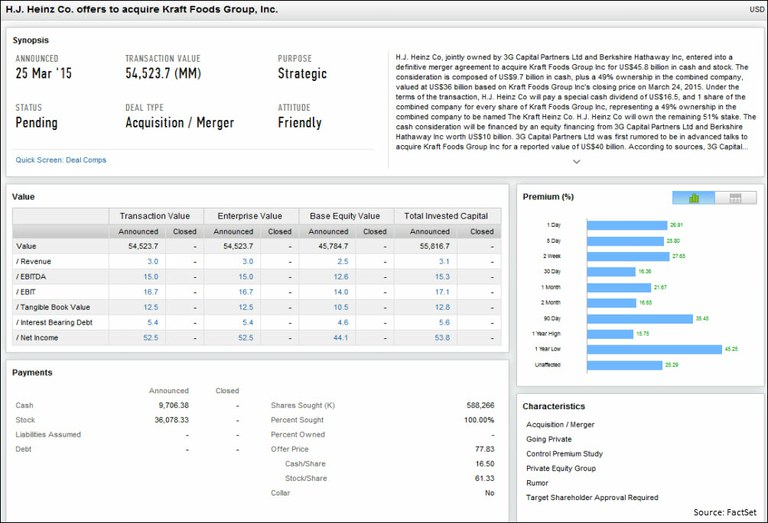

In March, H.J. Heinz Co. announced its intention to acquire Kraft Foods Group for $45.8 billion. The deal is comprised of roughly $10 billion in cash (financed by 3G Capital Partners and Berkshire Hathaway), plus a 49% ownership in the combined company, which is valued at approximately $36 billion. Heinz will also be paying a $16.50 special cash dividend to shareholders. The Kraft Heinz Company will be the fifth largest food and beverage company in the world, and the merger has been the largest M&A transaction to take place in the space in the past five years.

During an investor call on March 25 to review the merger and identify key opportunities for growth, management noted the potential for cost savings, estimated at $1.5 billion, a cornerstone of 3G Capital’s approach to long term investing. 3G is often known for its “zero based budgeting” approach, which requires yearly evaluations of expenses to eliminate wasteful spending. Alex Behring da Costa, President of H.J. Heinz Holding Corporation and Managing Partner of 3G, discussed the de-leveraging process by reducing leverage through paying down debt (“$2 billion of debt within the first two years after close”) and by not implementing share repurchases for at least two years following the close of the transaction. The combined Kraft Heinz Company’s commitment to investment grade capital structure will be a powerful storyline with Kraft on watch for a possible downgrade from both S&P (BBB) and Moody’s (Baa2).

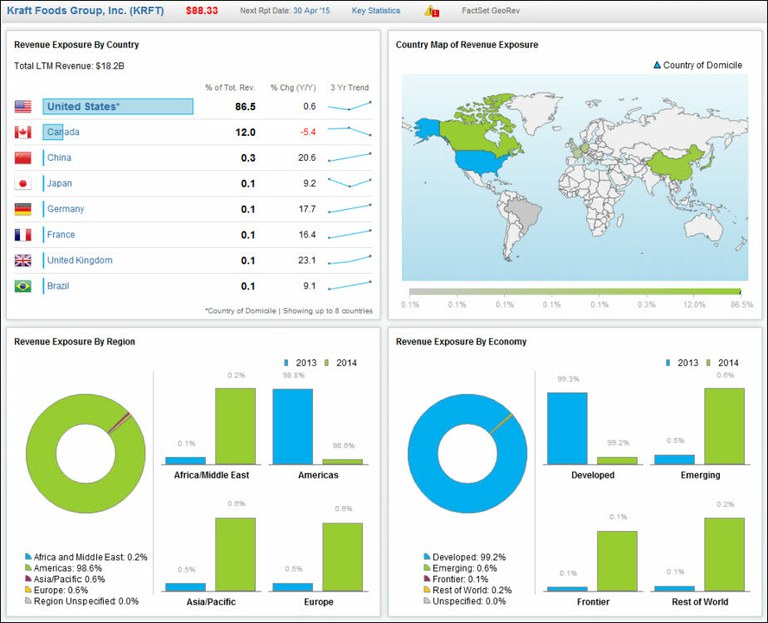

Kraft sales have declined for the past four years with increased competition from organic niche players. One of management’s stated priorities is to expose Kraft to the international markets. Currently, Kraft generates 86.5% of its revenues from the U.S. and only 0.6% from emerging markets. While this arena may be an avenue for growth, international consumer tastes are markedly different from the U.S. Targeting this international demographic may lead to higher costs in marketing, branding, and consumer surveys.

Consolidation is nothing new to the food and beverage industry, with over 380 mergers and acquisitions in the last five years. But the outlook for the Major Diversified Food industry is not promising. Sales estimates are below historical averages and EPS revisions have trended lower. So far in 2015, 54% of analysts (19) have revised estimates down and only 23% (6) have revised up.

Did Heinz pay too much of a premium for a company that is struggling to grow revenue outside of the U.S. and losing market share to healthier alternatives? Only time will tell, but analyst forecasts are certainly not promising for the year ahead.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.