There seems to be continued interest in Smart Beta, especially risk aware strategies such as minimum variance and low volatility. A second trend that we have observed recently among our clients is a shift towards more passive approaches to obtaining market exposure. One might be tempted to jump to the conclusion that active management is dead, or could we use these techniques in a reshaped form of active management?

We have looked at minimum variance before and although these strategies promise better risk adjusted performance, they confront us with some more operational types of risk - the portfolios end up being very concentrated and tilted towards low liquid names. In my previous article, Avoiding the void: Controlling for liquidity risk in equity markets, we saw that avoiding to buy or trade illiquid names proves to be a viable option. For this article, however, we’ll take a different approach and investigate whether we can deploy a strategy to a universe of ETFs. Investing in ETFs allows us to avoid liquidity and concentration concerns while obtaining global exposure with a few dozen securities in a portfolio rather than a few hundred. In this article, we will further generalize this idea and look at whether we can apply this method to other strategies, such as 1/n and volatility weighting.

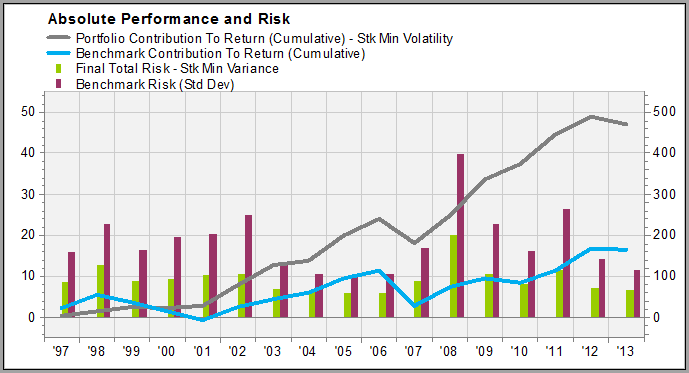

Let us first look at a typical minimum variance strategy. In the case below, we took a global universe and used an optimizer to construct a portfolio with minimal absolute risk.

As we see above we meet the first objective of minimizing risk, as the risk numbers are reduced by roughly 50%. Furthermore, we see a significant outperformance of 300% relative to the benchmark.

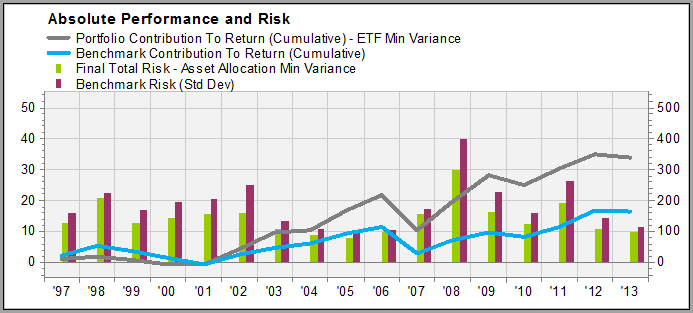

Now let’s have a look at the results when we change our buy list to a set of country ETFs and let the optimizer construct the portfolio instead of buying equities. A quick technical note, although ETFs are used as the investment vehicle, we’re applying look through and using this to our advantage to better estimate the diversification.

First, we see that the risk reductions are more in the 20% than 50% range, which shouldn’t come as a surprise now that we invest in ETFs and have only diversification at the country and not at the security level. More importantly the strategy still shows a very decent outperformance of roughly 200%.

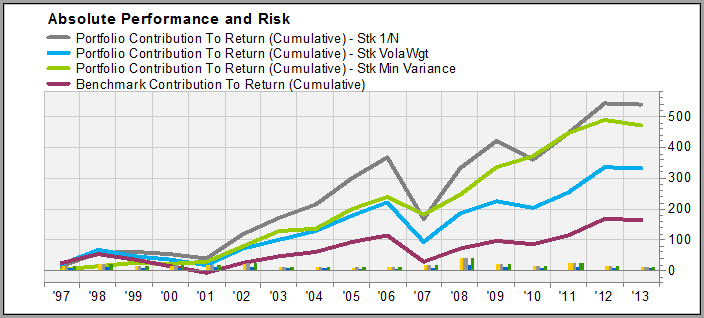

So, can we apply this method to other strategies as well? First, let’s have a look at 1/N and volatility weighting by applying it at the security level:

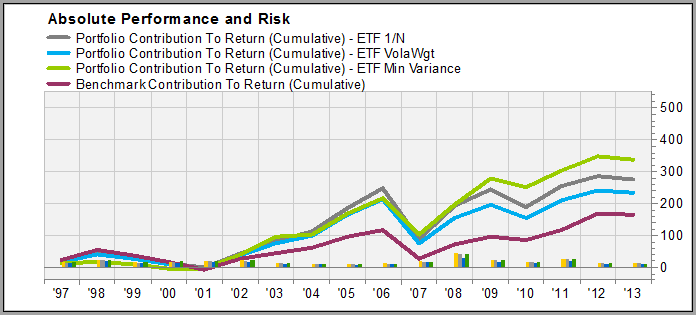

Then let’s look at the results when using ETFs as our investment vehicle:

Similarly to the minimum variance approach we see that the strategies show a somewhat muted but still strong outperformance compared to the benchmark. Perhaps we have found our answer to why there is so much interest in ETFs. Although these are considered passive, it is actually very possible to apply a very active strategy on top of them. The king of active management is dead, long live the king!

U.S. Mergers & Acquisitions Monthly Review: June 2026

U.S. Mergers & Acquisitions Monthly Review. Gain deep insights into market trends and expert analysis to inform your business...

What 2Q Bank Investment Gains May Signal for Insurance Results

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

Metals & Mining: Copper Capex Watch

FactSet metals and mining analysis: With copper pushed into fresh record territory, explore a capex intensity framework for...

Insurance: Macro Trends and Business Mix Expected to Shape 2Q Earnings Results

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)