U.S. Equity dominated November inflows, taking in over $49 billion in a month when net flows totaled $47 billion. U.S. Equity also dominated on a year-to-date basis, with 51% of all net flows.

Emerging markets and gold were hit hard after the Trump victory. Emerging markets equities and bonds lost 3.47 billion, 2/3 of those losses were from equity funds, with 1/3 from fixed income. Gold lost 3.45 billion, or 8.07% of AUM in November.

U.S. Financials picked up 6.86 billion, though the same cannot be said of leveraged U.S. financials, which actually saw outflows of $141 million in November. Direxion and ProShares, the largest issuers of geared funds, suffered $1.37 billion in outflows.

Treasury Inflation Protected Securities (TIPS) had a great month, with $2.55 billion in inflows. Broad-based TIPS funds increased AUM by 9.96%. This was in contrast to U.S. Government and Treasury funds, which saw $246 million in outflows. Inflation protection seems to have made all the difference for November.

And now for the fun part, where we use FactSet classification data to drill down and find trends in the November flows data.

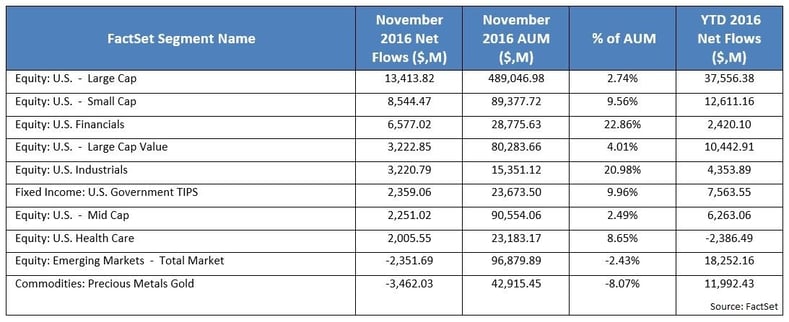

The table below—which shows all segments (FactSet’s ETF competitive landscape unit) with flows over $2 billion—displays the effects of November’s U.S. presidential election, which unleashed optimism in U.S. large caps (both broad based and value), small caps, financials, and industrials. U.S. TIPS also came up strong, as investors got a whiff of inflation in the Trump-scented air.

November’s biggest losers include emerging markets, as ETF investors shied away from exporters and gold, and a financial safe haven seemed less necessary.

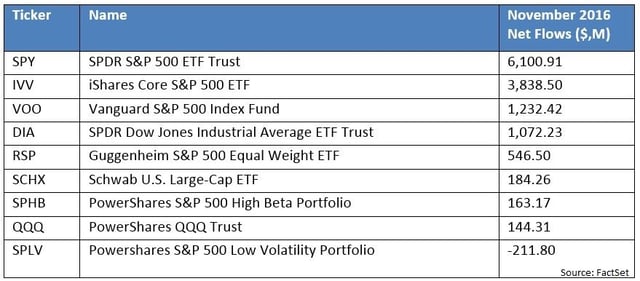

Digging deeper, it becomes clear that not all U.S. Equity funds benefitted equally from the post-election enthusiasm. Investors specifically sought out not just any large caps, but focused on S&P 500 funds. The table below shows all U.S. Large Cap funds with November 2016 flows over $100 million. The three S&P 500 funds, SPY, IVV, and VOO, captured $11.17 billion, or 83.2% of all U.S. Large Cap inflows.

That bottom line, showing SPLV’s outflows, the only significant outflow this month in U.S. large caps, is a story in its own right.

FactSet’s strategy field, which describes the selection and weighting process that drive index and fund construction, allows us to see that, during this banner month for U.S. equities, investors ditched U.S. low volatility and multi-factor funds, and not just in large caps. November marked a clear victory for plain vanilla index construction, across the U.S. equity space.

Vanilla U.S. Equity funds, funds tracking indexes that aim to represent the overall market, raked in $35.6 billion.

Low volatility funds saw $807 million in outflows, led by iShares Edge MSCI Min Vol USA ETF (USMV) and PowerShares S&P 500 Low Volatility Portfolio (SPLV).

Multi-factors were November’s second biggest losers, with $640 million of outflows in multi-factor funds, led by $1.12 billion outflows from First Trust Consumer Staples AlphaDEX Fund (FXG) and $1.09 billion outflows from First Trust Consumer Discretionary AlphaDEX Fund (FXD).

These AlphaDex outflows are not simply attributable to sector influences, as a quick look at the consumer segments shows. The U.S. Consumer Cyclicals segment gained slightly from flows, with $1.16 billion into the Consumer Discretionary Select Sector SPDR Fund (XLY) more than offsetting FXD’s outflows. Consumer non-cyclicals had outflows across the board, but FXG’s asset drain was 4.5 times larger than giant Consumer Staples Select Sector SPDR Fund (XLP)’s loss of $245 million.

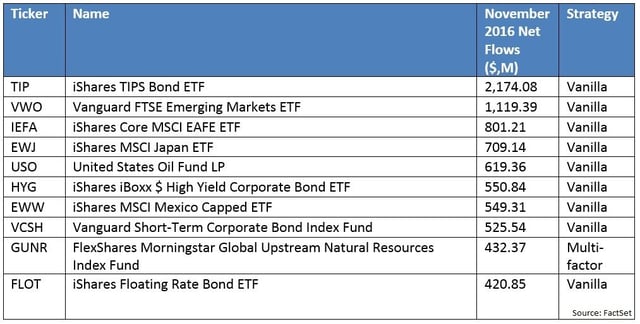

In fact, even outside of the U.S. equity space, vanilla funds dominated the inflows, as nine of the top ten gainers in the table below track broad-based, cap-weighted indices.

Funds like Vanguard FTSE Emerging Markets ETF (VWO), iShares Core MSCI EAFE ETF (IEFA), and iShares MSCI Japan ETF (EWJ) simply crushed the likes of iShares Edge MSCI Min Vol EAFE ETF (EFAV). EFAV lost $688 million to outflows this month.

Vanilla funds’ dominance was not necessarily uniform in emerging markets, developed markets (Ex-U.S.), or Japan.

Emerging market equity ETFs saw $2.01 billion in net outflows in November. Broad-based funds, cap-weighted VWO, and iShares MSCI Mexico Capped ETF (EWW) bucked the trend, though VWO’s gains coupled with EWW’s $549 million in inflows could not match iShares MSCI Emerging Markets ETF (EEM)’s $3.54 billion outflow. Tellingly, EEM, BlackRock’s flagship emerging markets trading vehicle responded to market sentiment, while their buy and hold oriented iShares Core MSCI Emerging Markets ETF (IEMG) actually saw minor inflows of $27 million.

In developed markets outside of the U.S., vanilla, value, and growth saw inflows of 1.71 billion (including iShares MSCI EAFE ETF (EFA)’s $206 million outflows), while currency-hedged and low volatility funds saw outflows of $1.27 billion.

Japanese equity ETFs saw inflows of $1.16 billion overall, distributed across a variety of strategies, though currency-hedged, multi-factor WisdomTree Japan Hedged Equity Fund (DXJ) did shed $94 million in November.

Insight/Author%20Bios/Elisabeth.jpeg)

Ms. Elisabeth Kashner is Vice President, Director of Exchange-Traded Fund Research and Analytics at FactSet. In this role, she develops tools and methodologies for all aspects of ETF and mutual fund classification and analysis with a focus on costs, risks, trading issues, and performance. Prior, she served as director of research at ETF.com and published extensively on the classification, efficacy, and persistence of strategic beta strategies and robo-adviser portfolio exposures. Ms. Kashner earned a BA from Brown University and an MS in financial analysis from the University of San Francisco. She is a CFA charterholder.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

Hyperscalers Tap External Financing as AI Capex Outruns Cash Flow

Explore this FactSet analysis of what is driving the funding shift among the five major hyperscalers plus implications for credit...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.