Royal Dutch Shell announced its offer to acquire BG Group in a friendly acquisition that carries a base equity value of just under $70 billion. The deal would be the second largest merger in the oil and gas industry with only the ExxonMobil deal with a value of nearly $77 billion carrying a larger value. The BP-Amoco deal, also in 1998 and third-ranked deal based on equity value, falls short of the Shell-BG deal by 31%. There are only three deals ever in the oil and gas industry with a base equity value of at least $35 billion, and the average for all deals in the industry is $482 million.

Commentary from Canaccord analyst Richard Griffith notes that Royal Dutch Shell does not appear to be overpaying in the acquisition, despite a 50% premium, if the long term valuation of BG Group is assumed to be $90 billion. Given the shock in oil prices, BG’s current market price may be temporarily depressed, given the premium is only 72% above the one-year low for BG stock. The premium above the one-year low price of the target company averages 123% for the oil and gas industry and was 91% during the 1998 wave of mega-deals.

The offer of $5.70 in cash and 0.4454 shares for every share of BG, in Shell B shares or possibly Shell A shares with approval from the Dutch Revenue service, will give BG shareholders a 19% ownership stake in the combined company. In addition to the approval from the Dutch Revenue service, Shell highlights necessary regulatory clearances related to the European Commission, Brazilian CADE, Chinese MOFCOM, Australian foreign investment, Australian antitrust, United States antitrust, as well as shareholder approval. Despite the litany of necessary regulatory filings and approvals, the deal is expected to be completed in early 2016. Shell already has unanimous support from BG Directors, but its holdings make up only 0.006% of BG’s issued share capital. Norges, the largest holder of BG stock, holds 5% of shares outstanding, and the top 10 holders have a combined 27.7% ownership.

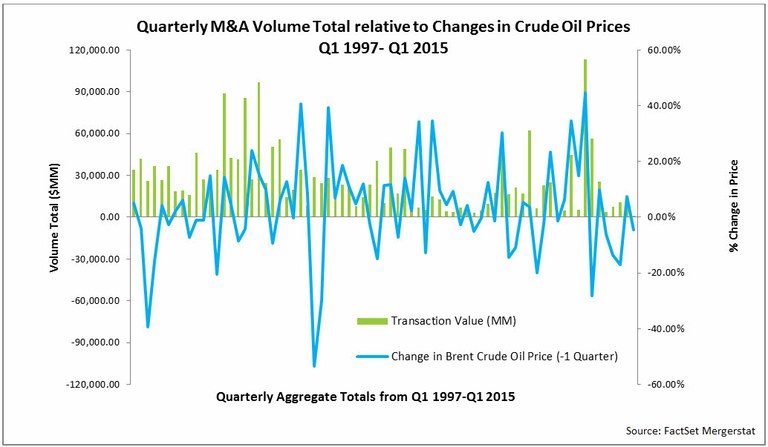

The general sentiment is that falling oil prices catalyze more M&A in the industry, both in terms of the number and size of deals, as stand-alone entities can no longer compete and larger companies, especially with the ability to finance the deals with low debt costs, can use acquisitions as a means to make strategic acquisitions for increased market share and provide a boost to revenue. The deal will grow Shell’s position in liquefied natural gas, which is a growth priority for the company that expects long-term rising demand in cleaner-burning fuel, and accelerate the rate of change of the company’s portfolio to match the new energy demands. Shell already derives about 75% of its overall income from L.N.G. and related businesses, and the BG acquisition is expected to increase capacity by 73% in the next three years.

Shell expects to concentrate its business model on fewer themes, but at a larger scale, to generate an increased cash flow. Shell also highlighted the priorities for the completion of the deal to be:

The deal should see an increase in cash flow from operations on a per share basis in 2016 which will allow the company to begin its share buybacks. As for synergies, Shell expects the deal to reach $2.5 billion per annum, with $1.5 billion from reduced exploration expenditure and $1 billion in operational savings, including efficiencies in market and shipping costs and operated procurement spend. The implementation of the combined operations, however, will come with a one-off cost of nearly $1 billion over a three-year period, with approximately 65% incurred in the first year post-completion. Shell expects the combination will be accretive to earnings per share beginning in 2017 and the accretion will grow from 2018 onwards. Reports from Jefferies analyst Jason Gammel predicts EPS dilution of 10% in 2016 and 4% in 2017; accretive by 7-9% from 2018-2020; stagnation after 2020 unless the entity can achieve additional synergies.

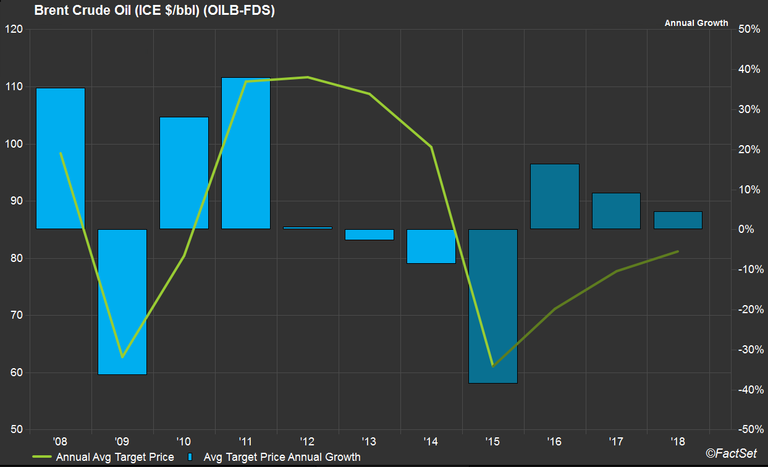

As mentioned in its recent 6-K, underlying Shell’s earnings forecast is a prediction of Brent oil prices to be $67 per barrel in 2016, $75 per barrel in 2017, and $90 per barrel from 2018-2020.

The price estimate is primarily tied to macroeconomic forecasts and demand growth. The forecast is also subject to risks and changes associated with currency fluctuations; risks of doing business in developing and sanctioned countries; legislative and regulatory developments including measures addressing climate change; physical and environmental risks; drilling and production results; reserve estimates; and market share and industry competition, with many analysts expecting Exxon to be next in line for a major acquisition.

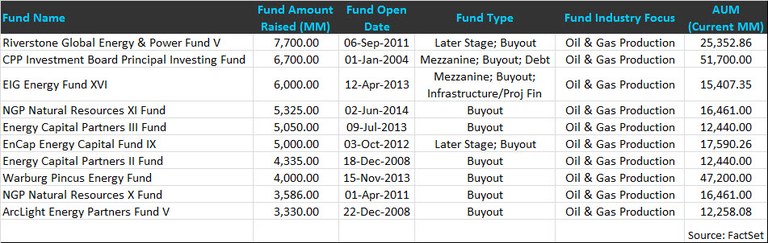

Private equity firms are also expected to be major players in the acquisition market. Since the beginning of 2014, there are 69 funds focused on the energy mineral industry in the capital raising or investing stage that have completed funding rounds for over $92 billion in new capital investments and have over $527 billion in AUM.

U.S. Mergers & Acquisitions Monthly Review: June 2026

U.S. Mergers & Acquisitions Monthly Review. Gain deep insights into market trends and expert analysis to inform your business...

What 2Q Bank Investment Gains May Signal for Insurance Results

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

Metals & Mining: Copper Capex Watch

FactSet metals and mining analysis: With copper pushed into fresh record territory, explore a capex intensity framework for...

Insurance: Macro Trends and Business Mix Expected to Shape 2Q Earnings Results

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.