Let’s make a deal! Except, not really. Instead, let’s play the game where we try to guess what Warren Buffett is up to next. This is definitely a well-worn game, and we will almost certainly be wrong, but games are meant to be fun! If the game analogy doesn’t work for you because winning is everything, then let’s treat this as a poor man’s thought experiment instead—clearly this is not going to be at the Schrödinger's cat level, but the process will (hopefully) be interesting nonetheless. And at the end of ours, we've identified eight companies we think are most likely to be Buffett's next target.

Anyone that has followed Berkshire Hathaway for more than five minutes has seen the acquisition criteria in its annual report. If for some reason you have not, here it is for reference:

We are eager to hear from principals or their representatives about businesses that meet all of the following criteria:

The larger the company, the greater will be our interest: We would like to make an acquisition in the $5-20 billion range.

This is the first and most important part of the puzzle, because we’re told almost exactly what Buffett wants. Ending the latest quarter with nearly $100 billion in cash and equivalents on the books, the $5-$20 billion range is grossly understated, especially given that Buffett has already mentioned possible transactions up to $150 billion, and Berkshire was a participant in the failed $142 billion Kraft-Unilever attempt earlier this year.

Now for the fun part. With more data, more sophisticated analytical tools, and fewer public companies, our odds of landing in the target zone are improved, even though our assumptions are by no means guaranteed. So let’s jump straight into the deep end and break down the criteria.

The only item we’re not able to filter is item six: an offering price. This is because we don’t know what companies are actually for sale and which may be shopping a deal to Buffett at the moment. That rounds out Berkshire’s stated criteria; however, there are a few other key items to factor in.

Given Berkshire’s acquisition history, we’re also going to limit our predications to companies that have a primary geographic revenue exposure to the U.S. using FactSet’s GeoRev data. Additionally, Buffett has recently been on the record stating India has “incredible potential” but suffers from excessive regulation.

With that in mind, we are excluding companies based in India. Buffett has a stated aversion to technology (see item five on his list), but he has purchased Information Technology Services and Prepackaged Software companies before, so we are not going exclude investment opportunity; we’ll follow his track record rather than his statements.

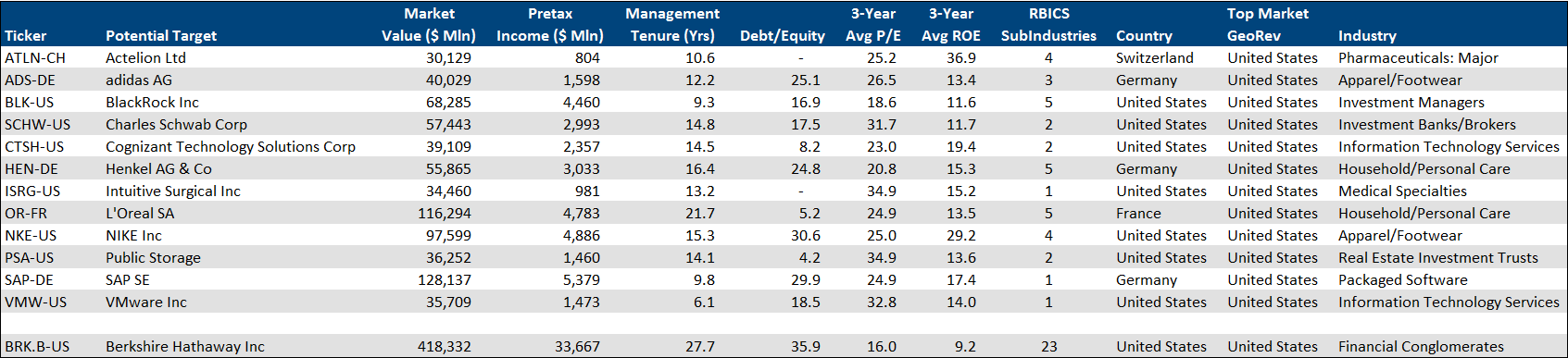

From the 83,000 public companies (273,000 securities) in our investable universe at the start, we are left with just 12 companies that meet all criteria.

Note that Berkshire is in our investable universe, and while we applied the same criteria, it failed to pass because its Debt/Equity ratio is 36% and it operates in a whopping 23 RBICS subindustries. Though this may not seem positive at first, we’re reminded of the old adage, “Do as I say, not as I do.” This means we could keep our criteria at the higher bar on the premise that Buffett is no longer looking to invest in Berkshire but rather on behalf of Berkshire and its shareholders. This is also one of the reasons why he doesn’t like share buybacks.

Our initial screening criteria results in the following 12 companies, with Berkshire added for comparison.

Before we get carried away, let’s look at the third part of the puzzle: what is the trading performance? Given the height of equity markets these days, if any of these appear inflated then we shouldn’t expect an investment from a value investor like Buffett. Charting one-year results, our initial list of 12 can probably be whittled down to eight by excluding Actelion Ltd, Charles Schwab Corp, Intuitive Surgical Inc, and VMware Inc, which are too expensive on a relative basis.

The fourth piece of the puzzle uses FactSet People and FactSet Ownership data to see if there are any other clues that can help us narrow the list of prospective acquisitons. Two things stand out from the eight companies we have left:

It would be difficult to imagine Buffett paying a CEO the kind of salaries Larry Fink ($25.5 million from BlackRock), Mark Parker ($47.6 million from Nike), or Ronald Havner, Jr., ($11.2 million from Public Storage) are being paid. Buffett’s annual total compensation is still just $487,881, and while its possible to overcome this compensation issues, those are some large gaps to fill.

L’Oreal, Henkel, SAP, and Nike all have significant insider ownership—at least 20% and upwards of 60%. L’Oreal in particular is challenging because Nestle currently owns a significant stake. Even with activist Daniel Loeb’s Third Point agitating for change at Nestle, (including a sale of its 23% L’Oreal stake), the position looks firm for now. Perhaps Buffett could “help” Nestle offload the stake, which would also help fend off Third Point. As with compensation, insider stakes is not an insurmountable hurdle, but a hurdle nonetheless.

In both of these issues, there are plenty of precedent cases in Berkshire’s historical deals. For example, as Chairman and CEO of Precision Castparts, Mark Donegan was paid $15.8 million, and both H.J. Heinz Co and WM Wrigley Jr. Co. had significant insider stakes prior to Berkshire’s acquisitions.

We are now at the last, unwritten, and perhaps most critical part of the puzzle. Unfortunately, we don’t have a way to model or screen on it though. Warren Buffett buys what he wants, and he requires a moat (said in less medieval terms: a competitive advantage). All of the companies in our result set look like viable candidates, but does Buffett think so, and do they have a business that appears unassailable? We have no idea.

These criteria can certainly be picked apart, massaged, and nuanced ad infinitum (and ad nausea), but that's the fun in this game: to see if you can land in the same company as the Oracle of Omaha, if only for a fleeting moment?

Hey, at least it we’re not roleplaying as Apple Inc., which still has no idea what to do with all its cash.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)