Pity the poor exchanges. Their business is getting companies and ETF issuers to list their products on their exchanges, and then convincing traders to execute their trades with them.

That's the business—they make money from listings, and from fractions of pennies based on volume. To do both these things, they have to convince the market that they make good markets—that trades happen in an orderly fashion without errors and hiccups.

In pursuit of this positioning, the New York Stock Exchange instituted a rule back in 2008 (approved by the Securities & Exchange Commission, and quickly duplicated by other exchanges) that allowed them to flag trades as being "aberrant."

Note that this isn't the same as actually cancelling trades. There's a separate rule for actually reversing trades that are considered "clearly erroneous." But both rules interact, and it's important to understand the unintended consequences of these kinds of rules before we consider whether the new rule is silly.

In all cases, the NYSE (and other exchanges, but I'm focused on NYSE right now) has the concept of a "reference price." The reference price is essentially the last-known "good" price for a security. Most of the time, this is simply the current national best bid offer (NBBO). If the exchange determines (for whatever reason) that the NBBO is also bad (say, it's 10 percent wide), then it can use the next trade that happens after the trade being assessed.

So we have a "bad" trade being measured against a "good" trade. Now it gets confusing. . .

Under rules adopted in 2008, the exchanges can already flag trades as aberrant. The guidelines are as follows:

| Stock Price | Aberrant If |

|---|---|

| $0-15 | 7% off |

| $15-50 | 5% off |

| >$50 | 3% off |

In other words, if your $40 stock has a print that's less than $38 right after the NBBO was $40, then it will get flagged on the tape as "aberrant" and it won't be marked as a high or low or even as the last or closing price for that security. The trade stands, but it "disappears."

A similar set of rules is used to break bad trades, but there are significant differences. The biggest difference is that nothing happens automatically. While the exchanges are happy to doctor the tape on their own, if you want to break a trade, you have to (as a member of the exchange) report your grievance in writing (on a Web form) within 30 minutes of the execution. But of course, you have entirely different breakpoints to worry about, because otherwise it would be too easy:

| Stock Price | Clearly Erroneous If |

|---|---|

| $0-25 | 10% off |

| $25-50 | 5% off |

| >$50 | 3% off |

The short story here is that the NYSE is proposing that for ETFs and ETNs, the boundary be 0.50 percent (if the price is over $100) or 50 cents (if it's under $100). This is obviously enormously more restrictive than the current system (over six times more restrictive, in most cases).

Here's the actual reasoning from the proposed rulemaking:

"The Exchange believes that these are conservative values that are much larger than typical ETF arbitrage bounds, as evidenced for example by bid/ask spreads, and therefore should only be exceeded in cases where it may be appropriate to mark a given trade as aberrant."

They go on to cite the spreads of two of the most liquid ETFs in the world—the iShares MSCI Emerging Markets ETF (EEM | B-100) and the Vanguard FTSE Emerging Markets ETF (VWO | C-88)—as trading at 0.03 percent spreads despite being proof that these 0.50 percent bands are "conservative."

There are numerous obvious problems with this proposal. The first is not all ETFs trade 3 cents wide. In fact, the median ETF trades about 20 basis points wide, with more than 300 having 45-day averages over 50 basis points.

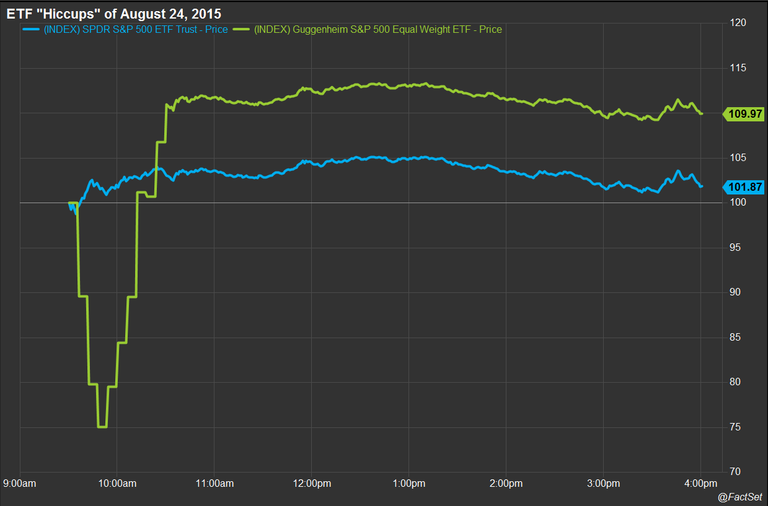

But the bigger problem is that bid/ask spreads often have nothing to do with price dislocations. During the hiccups of Aug. 24, many of the ETFs affected continued to advertise quite reasonable spreads, just at grossly depressed values.

ETFs can often trade at sustained premiums or discounts relative to the underlying for ages, for valid structural reasons (underlying securities can be closed, bond markets can lock up, issuers can close the creation window, etc.)

So basing the boundaries for what's "aberrant" on the bid/ask spread seems just odd to me. ETFs are often price-discovery vehicles. Arbitrarily limiting the advertised volatility of ETF trading to a 50 basis point band just seems wrong. A trade is a trade, after all. Either it's a bad trade, and should be actually reversed, or it's a good trade, and should be reported.

Like most rulemaking, the concern here isn't the intent as much as the unintended consequences. I have issues with the intent—it strikes me as whitewashing ETF trading to make exchanges look better—but the real issue is the long-term market impact. Once a trade is flagged as "aberrant," it gets removed from most reporting and most algorithms that analyze the market. It can affect volume weight average price, it can affect how institutions monitor their executions, and most troublingly, could significantly impact the closing price on a volatile day.

And as a thin end of the wedge, it strikes me that this reclassification of ETFs as having different rules would also inevitably spill into the "clearly erroneous" camp. Once that happens, it could have a chilling effect on ETF arbitrage.

One of the reasons that disconnects happen in ETFs is that despite seeing mispriced offers (or worse, market orders), most authorized participants (APs) won't step in and actually be the buyer of an off-priced offer during big market volatility. Why? Because they're in the business of staying flat. Whenever an AP buys 50,000 shares of an ETF, they're simultaneously selling some sort of hedge (often, all the underlying holdings).

And if they buy a 50,000-share lot "too cheap," the AP risks having half of their position broken (the "too cheap" lot) while being stuck with the other half (the hedge).

To be clear, that's not what the NYSE is proposing now. But for me, creating this "two camp" system, where ETF trading rules are fundamentally different than regular stocks, would almost inevitably lead to this problem.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)