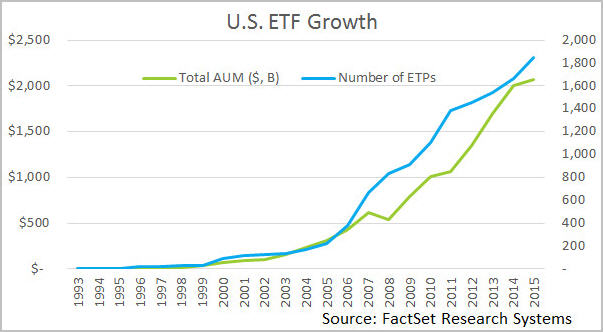

There’s little question that 2015 was a stellar year for the ETF industry. Assets are at all-time highs, and a record number of new ETFs hit the market.

Despite volatile markets, ETFs pulled in $242 billion in new assets—a number that looks even more impressive when you consider that traditional mutual funds hemorrhaged $125 billion in outflows. That's a $367 billion swing in a single year, away from an old technology and towards the hot new thing.

2015 was also a record year for ETFs in terms of new issuers coming to market. We had 23 brand new ETF issuers enter the market last year, ranging from startups with cool new ideas (HACK, anyone?) to old-guard firms like John Hancock and Goldman Sachs.

And while the big keep getting bigger—Vanguard and iShares branded ETFs pulled in $180 billion in new assets—many of the smaller ETF firms had huge growth years. Deutsche Bank, WisdomTree, First Trust, Schwab all posted asset gathering numbers over 25% for the year.

With all this great news, it's easy to look forward to 2016 with rose-colored glasses and think "well, things will be even better in 2016!"

And it might. But assuming so blindly and without caveats would be a mistake.

ETFs are a disruptive force, and that's got some folks scared. There's increasing mobilization to reign in, co-opt, and alter the course of the ETF revolution. We're at a pregnant moment of the ETF revolution; things could go any number of ways. As an investor—whether you're an individual, an advisor, a portfolio manager or an ETF issuer—you're going to be asked to take sides, and participate in shaping the future.

Here are the six things I think we all need to keep our eyes on:

These six topics are incredibly important, and how they shake out in 2016 is going to fundamentally alter the ETF market. I’ll be digging into each of these in more detail in my research this coming year, and I’ll start by presenting more details and some initial suggestions on how different kinds of investors can help prepare for these changes…and for the ambitious, move things in the right direction.

Join us at the Inside ETFs conference in Hollywood, Florida later this month to learn more about this topic.

It’s going to be an interesting year.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)