The shift away from defined benefit pensions to employee-driven defined contribution retirement plans has led to a population of employees who are often unsure of what to do to be ready for retirement. Many are turning to investment advisors for advice, and one of the biggest areas where an investment advisor can help clients is overcoming the behavioral biases and bad habits that can prevent them from being truly prepared for retirement.

Especially with younger clients, one of the hardest issues that advisors have to address is their clients’ natural tendencies to under-fund their retirement accounts. Since many companies offer 401k match, it can be easy to convince an investor that not taking advantage of the company match is the equivalent of giving away free money. It is much harder to convince an investor that saving above and beyond the “matched” percentage is worthwhile. After all, who wants to save money for a retirement that may be 30 or more years off at the expense of instant gratification and higher spending levels now?

For advisors, showing clients a Monte Carlo forecasting simulation that incorporates client-specific cash flows can really drive home the impact of different spending and saving levels on an investor’s retirement nest egg. Making a few basic assumptions about long-term capital market expectations and using a broadly diversified portfolio, the potential future outcomes of today’s savings choices become evident.

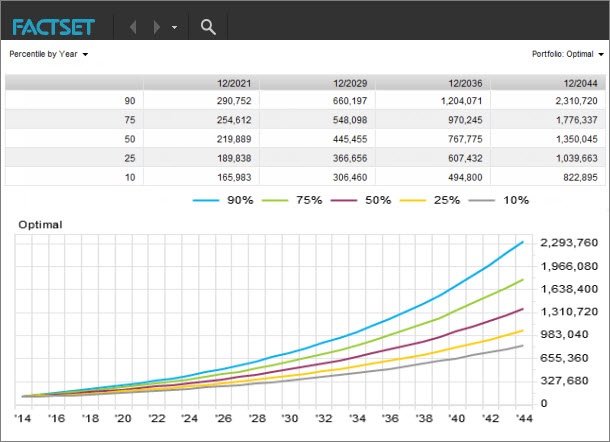

As an example, we’ll first look at a 30-year-old investor Steve, who is hoping to retire at age 60. Steve makes $100,000 and is planning on contributing the amount that his company will match, 4%, giving him a total annual contribution of $8,000. We’ll assume his salary (and contribution) grows at 3% a year and that his beginning retirement savings are also $100,000. As Steve and his advisor can see, the Monte Carlo simulation produces a range of possible outcomes, with the 50% value forecasting that Steve will have developed a retirement nest egg of $1.35 million.

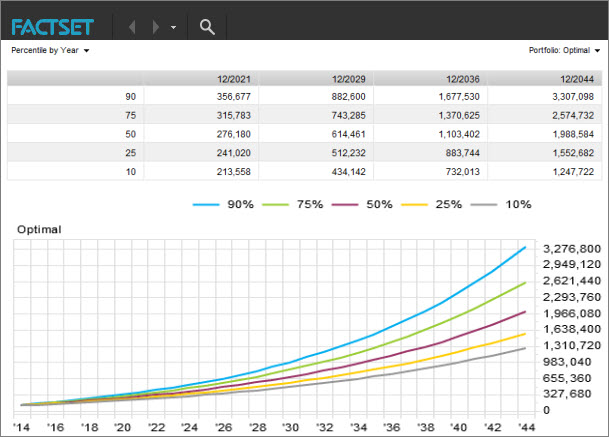

Let’s compare this outcome to Jill, an investor in the same boat as Steve but who is contributing 10% of her annual salary instead of the 4% he is saving each year. Using the same asset allocation forecast, Jill’s 50% terminal value is just under $2 million, which is more than $600,000 higher than Steve’s. At the 90% outcome, Jill will have saved over $3.3 million for retirement, while Steve was only able to reach a best case scenario terminal value of $2.3 million, a million dollars less than Jill!

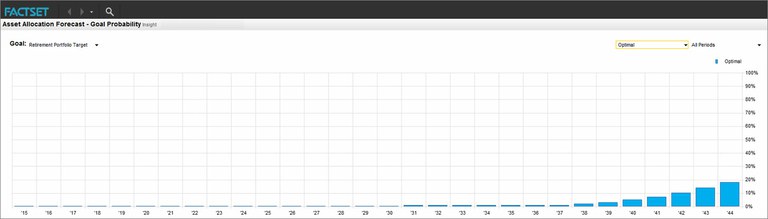

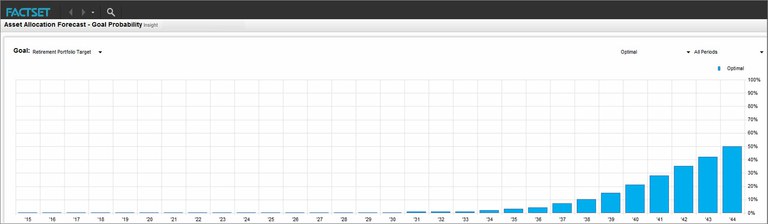

Finally, let’s assume that both Jill and Steve had decided with their investment advisors that the magic number they needed to hit in their accounts to feel comfortable retiring was $2 million. We can compare the probability charts for both Jill and Steve to see that Jill has about a 50% chance of achieving that goal, while Steve’s portfolio would achieve that outcome less than 20% of the time.

There are many places where an investment advisor can add value to an individual investor; however, one where they can have the largest impact is helping shape their clients’ behaviors when it comes to saving for retirement. Demonstrating the future impact of today’s decisions through an asset allocation forecast can help an investment advisor get their clients on the right track for retirement.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)