The U.S. equity market started 2016 with to the worst start to a year ever. Oil prices continue to tumble from the 2014 peak, without a bid (or production cuts) anywhere in sight. China is landing. . . although whether it is soft or hard is anyone’s guess. And the rest of the world continues to ease, with a new round of QE in the Eurozone, negative rates in Japan, and currency devaluation across the developing (and developed) world. On the horizon we have the Brexit referendum, the U.S. Presidential election, and the potential for continued macroeconomic divergence.

Given that backdrop, a continuing low interest rate environment, and struggles with liquidity, I have to ask the question, “What’s a bond investor to do?” The notion that return of capital is more important than return on capital holds true now more than ever. What I hope to shed light on is how a bond investor can view exposure to geopolitical risk, get back to the fundamentals instead of chasing yield, and integrate future economic expectations into their analytical process.

Geopolitical Risk

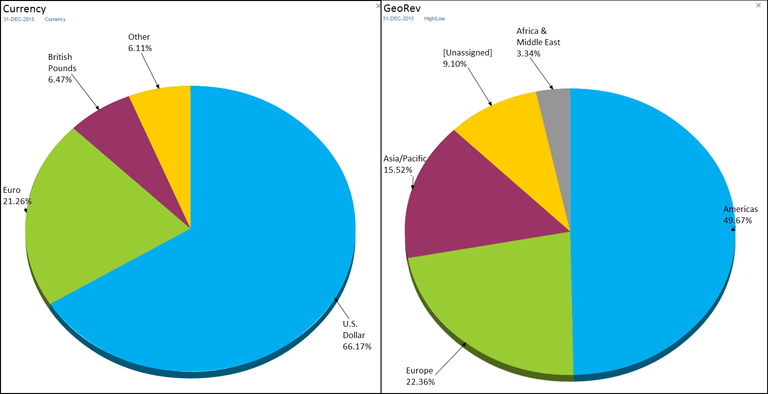

We work, play, and invest in an environment that continues to grow more interconnected globally. Traditionally country exposure has been based on country of domicile, incorporation, or exchange. That definition worked for a time, but as companies and economies have grown and technology has evolved, measuring geographic and geopolitical risk has become increasingly complicated. In the fixed income space, this exercise is further impacted by project-specific securities and complex corporate debt structures. I would argue that determining where your credits generate their revenue is a more fruitful exercise to determining geographic risk exposures. Using a global corporate bond index as our universe, I’ve applied FactSet’s GeoRev methodology in an attempt to gain further insight into geopolitical risk.

Not to overplay my hand too much (I still want you to attend my webcast!), but the analysis shows a much different risk picture than a region, domicile, or currency grouping portrays. I think you’ll be surprised by the outcome. I know I was. It would be interesting to go one step further and apply it to your firm’s book or individual mandates that are typically more concentrated than a broad index and see how the risk profile changes.

Fundamentals Are Paramount

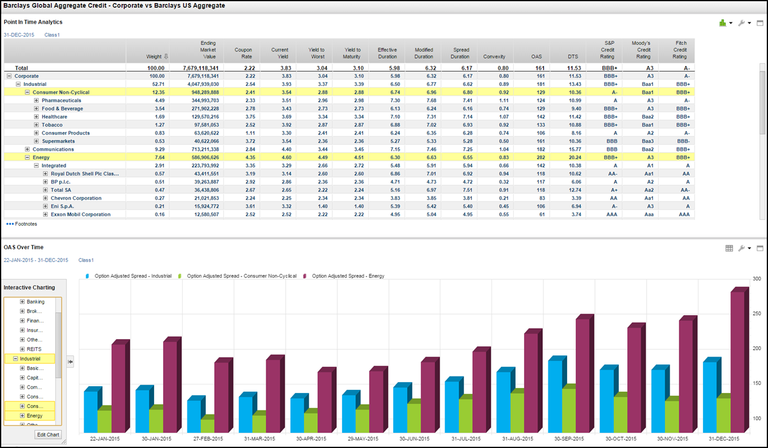

Once we’ve determined where we’re invested, it’s time to get back to fundamental analysis. Using our Portfolio Analysis application, I combined point-in-time analytics with a time series analysis on Option Adjusted Spreads (OAS). Spreads have widened over the past year, which is not news. However any weakness in the credit market is clearly not broad based. It’s startling to see how specific industries have behaved over the most recent year in the investment grade space (I also ran this using a global high yield index with similar results). Next, I looked at spreads historically going back to the bottom of the financial crisis. The tagline I’ve been using is an oldie but a goodie…"This time is different!” I think that you’ll find this piece interesting. Is there value in certain industries now, or only potential for more pain?

To take a deeper look, I combined issuer level fundamentals with our global index using FactSet’s entity data mapping and fundamental databases. Pulling in valuation measures typically seen in the equity space along with credit metrics like liquidity and solvency ratios helps to add a top down perspective. Running a similar time series analysis helps to validate the notion that for many issuers (and consequently, their issues) much of what we’re seeing now in the credit space has been a long time coming.

Impact of Known Unknowns

The final piece to the puzzle is thinking about how to overlay our macroeconomic expectations on our current portfolio. I utilize two specific tools here: interest rate scenario analysis and our simulation based risk model to view downside risk and stress specific factors in our global multi-asset covariance matrix.

In terms of interest rate scenarios, I thought about a bear flattener (what we are seeing now in the US), a 75 basis point move over the next year (which fits with a still somewhat consensus view that the Fed can raise rates three times in 2016), and a tightening of spreads in the Energy space (with the notion that the sector is oversold…and yes, I know that many of us have been running this analysis for over a year now). Reviewing results over 3, 6, and 9 month horizons provides a few interesting takeaways, perhaps the main one being that we shouldn’t fear US liftoff as much as the headlines would have us believe.

Using our simulation based analysis, I look to identify downside risk measures and apply factor stress tests. On the downside, viewing the global corporate universe gives us somewhat expected results in context of the portfolio, given the current macro environment. Looking through the lens of a marginal or standalone risk measure however gives us unexpected (at least to me) results. Stressing the portfolio using two globally applicable factor shocks provides further insight. Again I took the view of the overall portfolio context and a standalone basis, while looking at industry and issuer specifics.

Thinking about how these approaches would translate to your mandates, I can’t help but be interested to see how the output would look using a more concentrated portfolio constructed via an active approach.

In Conclusion

I used several unique tools and datasets to slice and dice a global corporate benchmark. We devised a new way to view geopolitical risk, tied fundamental issuer analysis back to the underlying credits, and then incorporated ex ante views onto the broader universe. What does all of this tell us? You’ll have to tune in to the webcast to get the details!