Over the last year, we've witnessed Fed rate cuts, technological advancements, and market headwinds that have affected the financial industry in myriad ways. In this article, FactSet's experts weigh in on the trends that have left their mark in 2019.

Sara Potter, Vice President, Associate Director, Thought Leadership and Insights

As we began 2019, the big economic stories were the Fed’s ongoing series of interest rate hikes (four in 2018), the ongoing U.S. government shutdown, the December 2018 stock market drop (S&P 500: -9.2%, DJIA: -8.7%), and the escalating U.S.-China trade war. As the year progressed, we saw movement on all fronts.

Sara Potter, Vice President, Associate Director, Thought Leadership and Insights

The big IPO story this year was the disappointing performance of several much-anticipated technology IPOs. Coming into 2019, the market was anxiously awaiting initial public offerings for the next generation of tech stocks, which included Airbnb, Lyft, Peloton, Pinterest, Slack, Uber, and WeWork. While Pinterest’s stock performed well following its IPO in April, a disappointing third-quarter earnings report now has the stock trading below its offer price. On the other hand, Peloton had a lukewarm market reception immediately after its September IPO, but the stock has surged as we entered the holiday shopping season.

The other tech IPOs have not fared as well. As shown in the table below, the IPOs for Lyft and Uber have all been followed by significant price declines. Even Slack, which went public via a direct listing, has underperformed (note that the reference price was $26.00 but the stock opened for trading at $39.50).

|

Company |

IPO Date |

Offer Price |

Price as of 13-Dec-2019 |

Price Return |

|

Lyft, Inc. |

28-Mar-2019 |

$72.00 |

$46.75 |

(35.1%) |

|

Peloton Interactive, Inc. |

25-Sep-2019 |

29.00 |

31.53 |

8.7% |

|

Pinterest, Inc. |

17-Apr-2019 |

19.00 |

17.45 |

(8.2%) |

|

Slack Technologies, Inc. |

19-Jun-2019 |

26.00 |

21.39 |

(17.7%) |

|

Uber technologies, Inc. |

09-May-2019 |

45.00 |

28.49 |

(36.7%) |

The market is no longer interested in overpaying for companies that have yet to turn a profit. Investors are demanding to see growing revenues and a path to profitability as well as a solid leadership team. WeWork (The We Company), a shared office space company, pulled its planned IPO in September in the face of intense scrutiny after it reported $1.37 billion in losses in the first half of 2019. Shortly afterward, the CEO stepped down; it is unclear if or when the company will go public. The highly anticipated Airbnb IPO is now expected to take place in 2020 but it appears that this will happen via a direct listing, following the paths of Slack and Spotify.

John Butters, Vice President, Senior Earnings Analyst

The estimated (year-over-year) earnings growth rate for the S&P 500 for CY 2019 is 0.3%, which is below the 10-year average (annual) earnings growth rate of 9.1%. If 0.3% is the actual growth rate for the year, it will mark the lowest annual growth rate for the index since CY 2015 (-0.6%). Six sectors are projected to report year-over-year growth in earnings, led by the Health Care and Utilities sectors. Five sectors are expected to report a year-over-year decline in earnings, led by the Energy and Materials sectors. S&P 500 companies with more international revenue exposure are expected to report lower earnings in CY 2019 relative to S&P 500 companies with less international revenue exposure.

For more details, please refer to my CY 2019 Earnings Preview.

Insight/2019/12.2019/12.13.2019_EI/S%26P%20500%20Earnings%20and%20Revenue%20Growth%202014-2019.png)

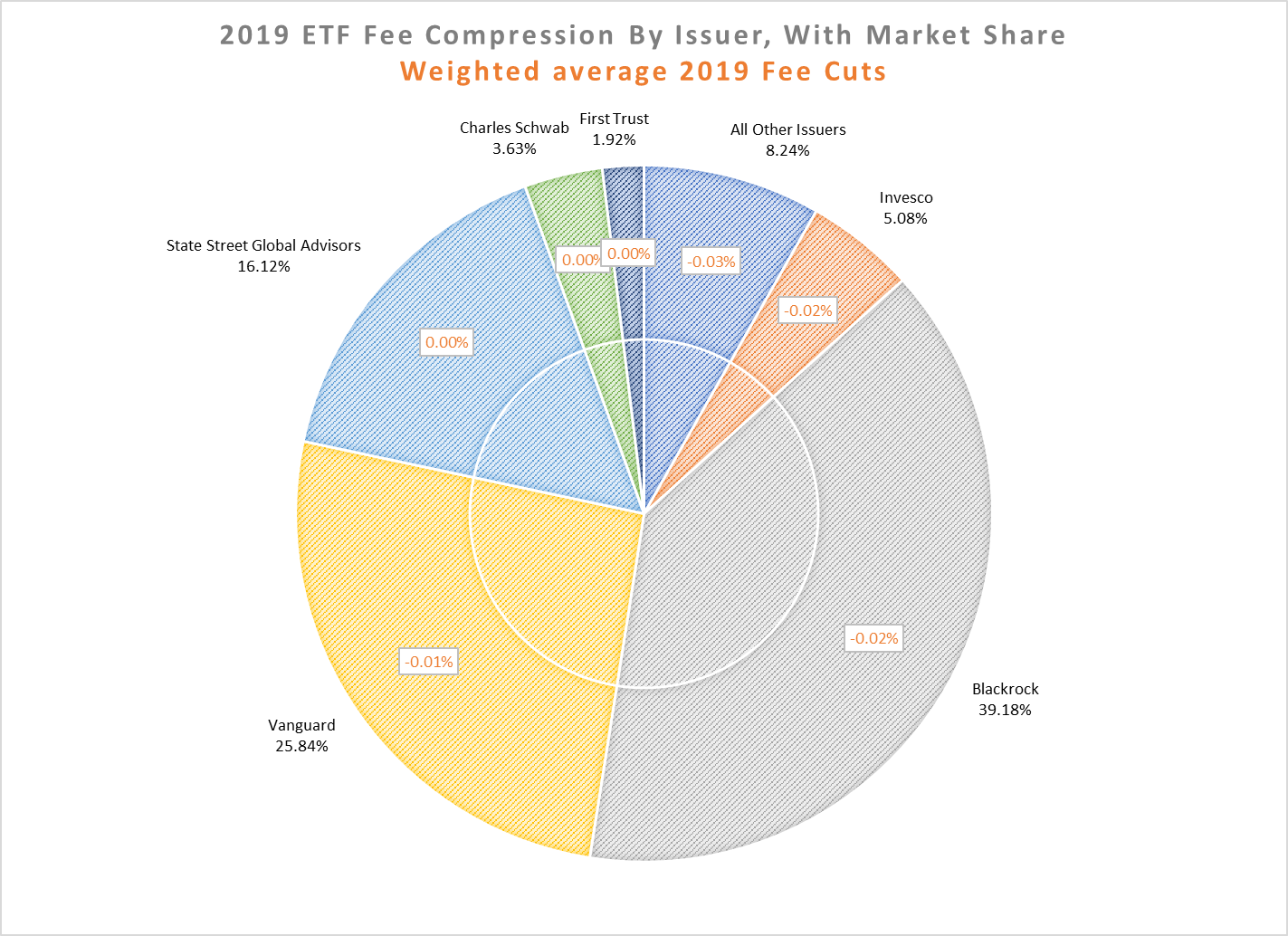

Elisabeth Kashner, CFA, Vice President, Director ETF Research

Concentration: six asset managers control 92% of all ETF assets. The others—all 118 of them—are fighting over 8% of the assets. The top two, BlackRock and Vanguard, manage two out of every three ETF dollars in the U.S.

Fee compression: asset-weighted average expense ratios dropped again in 2019. For the industry as a whole, expenses dropped from 0.21% at the end of 2018 to 0.20% as of December 15, 2019.

Pat Reilly, Vice President, Fixed Income Analytics, EMEA

The key trend/biggest surprise was the Federal Reserve seemingly buckling to political pressure and cutting interest rates three times during the year. With other central banks around the world following suit, risk asset returns were juiced, potentially pulling 2020 and beyond returns into 2019. In my opinion, this only serves to further inflate existing asset bubbles and push a long overdue inflection point into the future.

Barrie Ingman, Vice President, Principal Content Manager

In this piece last year, we correctly predicted a new Pan-European Personal Pension Regulation, intensified clamor around LIBOR transitioning, revamps to the EU banking prudential (IFD, IFR, CRD V, etc.), and EMIR derivatives (EMIR Refit and EMIR 2.2) regimes. Somewhat optimistically, we also predicted changes to MiFID II and some form of definitive Brexit development. While several developments in these areas did occur (multiple MiFID II tick-size regime modifications, Brexit-driven UK CCP and CSD recognition from the EU, a solid mandate for Brexit following the UK general election, etc.), these issues have largely leaked into 2020 and in retrospect, this might have been predicted.

We also correctly predicted further ESG and Capital Markets Union initiatives in the form of a Climate Benchmark Regulation, a Sustainability Disclosure Regulation, a Covered Bond Directive and Regulation, and new securitization-related measures (e.g., the delegated regulation on homogeneity of underlying exposures)—all just in time for Christmas. This being said, the first true EU ESG development sneaked under the radar much earlier in the year in the form of the sustainable investment accountability rules in the Second Shareholders Rights Directive. Finally, we also predicted an uptick in MiFID II related enforcement activity. However, as reported in our August Update, this failed to materialize; presumably, because regulators remain as overwhelmed as the market with the sheer breadth of the new regime.

Notwithstanding our overall prescience, we failed to predict the sheer scale of AML/CFT material that came gushing out of the doors of every EU political institution over the summer and also the surprising volume of SEC rule changes that emerged, which included the emasculation of the Volcker Rule, a neat example of the broader, cross-sectoral Trumpian deregulation agenda that occurred throughout the year.

In summary, it was a mixed bag of the expected and the unexpected but with a consistent trend of politically-driven developments and the perennial modification of existing regimes. The only true revolution was the EU ESG texts, which are just the tip of that particular iceberg.

Philipp Zerhusen, Vice President, Director of Market Development

Looking back at 2019, it was surprising how the discussion and hype around “Robo Advisory” literally fell off the cliff. While it was the dominant topic in my area of expertise in 2017/2018, it was almost a non-entity in 2019. I don’t believe this is due to “Robos” being any less relevant but rather having reached “mainstream status” with every financial institution now offering robo advisory in some shape or form.

In addition, ESG has arrived for private banking and wealth management. We shall see much more of this in 2020 and beyond.

Peter Davaney-Graham, CFA, Vice President, Head of Open:FactSet Content Strategy

2019 saw the early emergence of data science approaches across the spectrum of investors beyond the systematic traders and quantitative managers who have been the traditional users of these approaches.

Reinsurance Purchases Could Signal a Soft Market Ahead

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The Gilded Age: Examining Sectors of Gold, Mining, and Demand in the Past Decade

Explore FactSet Cobalt analysis of how each gold sector has reacted to price changes in the past decade. Read our key takeaways...

Explore the STOXX 600 Q2 earnings season with analysis from the StreetAccount European Macro Team at FactSet, including beats,...

Insurance: World Cup Exposure to Claims?

Stay ahead with FactSet’s weekly insights on the latest insurance industry updates, trends, events, and market developments.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.