The opinions expressed in this article are not legal advice and should not be relied upon as such.

If you are a supervised entity that makes use of benchmarks, you want to know two things: what do I need to do to comply with the BMR, and when do I need to do it? If you’re reading this article, you probably know that BMR refers to the new EU Benchmarks Regulation, (but if you’re unfamiliar with the regulation, you can read the text of the BMR).

The cheeky answers to those questions are “Not as much as you might think” and “No one’s quite sure.” However, the sober answers are that the amount of effort involved in compliance will vary significantly depending on the circumstances of individual benchmark users, and the BMR’s rules apply as of January 1, 2018, though they are tempered by a transition period that ends January 1, 2020.

The new mandates applicable to benchmark users can be summarized as two main requirements:

For many readers, the phrase “more easily said than done” likely comes to mind, but the summarized version of the rules, above, may help to focus your compliance efforts. So much for the “not as much as you might think” answer. What about the timing of compliance obligations?

The Article 28(2) benchmark contingency plan is not subject to the transitional provisions, meaning it must be complied with soon—January 1, 2018, the date on which most of the BMR’s rules begin to apply. A logical prerequisite to a benchmark contingency plan is to create an (updatable) inventory of the benchmarks one can “use” (see the section: “On the Many Uses of Benchmarks and the Use of Many (Blended) Benchmarks”).

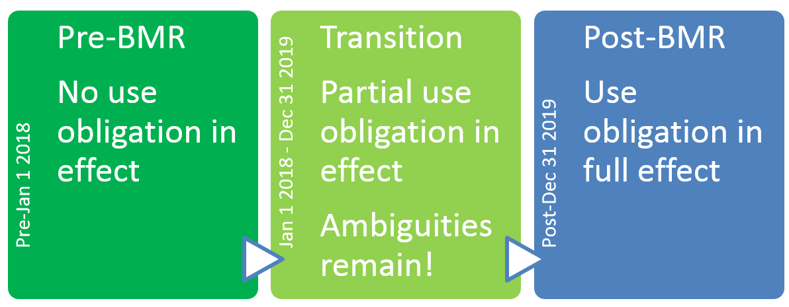

In contrast to the Article 28(2) requirement (the benchmark contingency plan), the scope and timing of the “use obligation” (as I like to call it, in a nod to the Markets in Financial Instruments Regulation’s trading obligation and European Market Infrastructure Regulation’s clearing obligation) is subject to the transitional provisions, meaning there is a phase-in effect. At first, compliance with the use obligation will be relatively easy (one can imagine initially using a manual approach to compliance), but over time it will develop into a challenge calling for an automated solution.

Between December 31, 2017 and January 1, 2020, in order to fully benefit from the transition period’s intended cushioning effect, the benchmark user will want to know whether a given benchmark is provided by an EU administrator or a third country administrator. If the former, the user will want to know whether the relevant EU administrator began providing benchmarks prior to the BMR’s entry into force or not (and, if not, whether the relevant administrator is in the European Securities and Markets Authority (ESMA) register); if the latter, the user will want to know whether the relevant benchmark was in use in the Union prior to January 1, 2018. Further considerations can come into play, but before losing the forest for the trees, let’s survey the forest a bit.

The phase-in of the use obligation can be represented as follows:

Benchmark users might be concerned they will need to drop unapproved benchmarks like a hot potato on January 1, 2018 and start using only those benchmarks listed in the ESMA register. Such is not the case. The point of having a transition is to minimize disruption to users. What’s more, the ESMA benchmark register will be empty on January 1, 2018 and, theoretically, it could remain empty throughout the entire transition period. Practically speaking, this is unlikely to happen, but it’s important to recognize that the ESMA register will be populated over time—even into the post-BMR period in the case of current administrators who apply for authorization or registration at the very end of the transition, as the rules permit.

When inventorying benchmarks, it is important to bear in mind that not every literal “use” of a benchmark constitutes legal “use of a benchmark.” The BMR’s definition of “use of a benchmark” contemplates only five modalities of use that count for purposes of the regulation. For example, holding a financial instrument that references a benchmark is not use of a benchmark. As a counterexample, blending benchmarks to create a rate for purposes of officially measuring fund performance is use of the benchmarks so combined, and the fund manager should include the relevant benchmarks in their benchmark contingency plan inventory.

One can speculate whether the rate determined by blending benchmarks is itself a new benchmark, transforming the ostensible benchmark user into a benchmark provider via a bit of legal alchemy! While entertaining to ponder, this is not the case. Such uses of combined benchmarks—blending benchmarks to measure fund performance, for example—are considered an “indirect” use of each of the constituent benchmarks, which accounts for the references throughout the BMR to “the benchmark [that] is used directly or indirectly within a combination of benchmarks.” Additionally, the cumbersome phrase “benchmark or a combination of benchmarks” is ubiquitous in the BMR since the rate determined by combining benchmarks is not, ipso facto, a benchmark.

Perhaps the most important point to make right now is that the rules during the transition are potentially quite generous from a user’s compliance standpoint, but ambiguities remain. In its 30 March 2017 Final Report, ESMA noted, in wonderfully understated fashion, “[T]he transitional provisions allow for (at least) two readings….” The parentheses around “at least” appropriately highlight the convolutions a diligent reader is put through in attempting to settle on a plausible and practical interpretation of the Article 51 transitional provisions.

Partial guidance about the transitional provisions has been published since the Final Report, but a number of wrinkles remain to be ironed out. Look for an upcoming Insight article specifically addressing the transitional provisions from the perspective of a benchmark user.

Mr. Nels Ylitalo is Director of Product Strategy for Regulatory Solutions at FactSet. Previously, he worked in signals intelligence in the United States Navy prior to attending law school at Yale where he earned a JD in 2007. Following law school, he was a corporate/M&A attorney representing VC and PE funds as well as corporate clients in M&A transactions. Mr. Ylitalo’s portfolio covers a broad range of financial services regulations with a current focus on buy-side regulatory requirements and challenges, globally.

SEC Adopts Amendments to the Names Rule under the Investment Company Act of 1940

On September 20, 2023, the U.S. Securities and Exchange Commission (SEC) adopted amendments to Rule 35d‑1 (the “Names Rule”)...

Demystifying the SEC’s Latest Update to the FAQ of The Marketing Rule

The SEC Marketing Rule was put in place to modernize marketing requirements for investment advisors. The latest update to the...

Uncovering Climate Transition Risk in EU Sustainable Finance Regulation

Sustainability (ESG) risk is a broad new regulatory concept prevalent in EU financial services regulation. Specifically, climate...

Learn about the most important compliance and regulatory news developments courtesy of FactSet's Regulatory team.

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.