In the latest projections published in the International Monetary Fund’s (IMF) October 2016 World Economic Outlook (WEO), the outlook for global economic growth was revised down slightly from the organization’s April forecast. The global economy is now expected to expand by 3.1% in 2016 and 3.4% in 2017, both numbers 0.1 percentage point lower than what was forecast in the previous publication. The downward revision reflects a weaker outlook for advanced economies in light of the UK Brexit vote and US economic growth that has fallen below expectations.

FactSet clients: launch this chart

However, the global growth projections mask two very divergent growth paths: a weak one for advanced economies and a more robust one for emerging markets and developing economies. The IMF’s forecast for advanced economies predicts 1.6% growth this year, followed by 1.8% in 2017 and 2018. This compares to a 4.2% growth rate in 2016 for developing nations, followed by acceleration to 4.6% in 2017 and 4.8% in 2018.

Growth in emerging economies is being led by emerging and developing Asia, especially India. The Indian economy expanded by 7.6% in 2015 and similar growth is expected in 2016 and 2017. Even as economic growth has been accelerating for the last three years, overall inflation has fallen, prompting the Reserve Bank of India to gradually loosen monetary policy.

FactSet clients: launch this chart

Starting in January 2015, the bank trimmed the repo rate by a total of 175 basis points, taking the policy rate from 8.0% to 6.25%; the most recent easing move was a surprise 25 basis point rate cut earlier this month. September 2016 inflation numbers released today show that consumer price inflation fell to just 4.3% last month, the lowest year-over-year price increase in a year. Currently, analysts surveyed by FactSet expect the repo rate to remain at 6.25% through 2017, but continued easing in prices could increase the probability of further rate cuts.

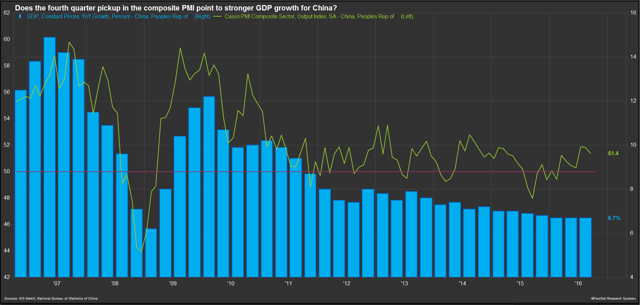

Meanwhile, even though China’s growth deceleration is expected to continue for the next few years, the relative strength of the world’s second largest economy is still a key driver for growth in emerging Asia. Last year’s 6.9% growth rate was the slowest pace in 25 years; the IMF is forecasting further slowing ahead, to 6.6% in 2016, followed by 6.2% in 2017 and 6.0% in 2018 and 2019. The 2016 growth forecast is consistent with the government’s growth target range of 6.5% to 7.0%; the economy expanded by 6.7% in the first two quarters of the year, and next week’s release of third quarter results will provide more information on performance in the second half of the year.

FactSet clients: launch this chart

The Caixin composite PMI for China, which includes both the manufacturing and services sectors, averaged 50.4 in the first half of the year, just barely above the 50 threshold that indicates expansion. The index averaged 51.7 in the third quarter, signaling a potential pickup in GDP growth, although FactSet Estimates currently show an expected year-over-year growth rate of 6.6%.

As for the UK, the IMF has significantly reduced its growth forecast in the wake of Brexit. The April publication projected 1.9% growth in 2016 followed by 2.2% in 2017; these numbers have now been revised down to 1.8% and 1.1% in 2016 and 2017, respectively. The downgrade in the US forecast for 2016 reflects the slower path of economic growth seen in monthly indicators since April; the IMF is now forecasting 1.6% growth this year followed by 2.2% in 2017. The IMF’s 2016 and 2017 forecasts for the US are consistent with analysts surveyed by FactSet; however, the FactSet survey shows much higher pessimism for the UK economy in 2017, with growth projected at just 0.8%.

FactSet clients: launch this chart

The challenge will be for these countries’ respective central banks to navigate monetary policy through these slowdowns; continued accommodative policies will likely persist, even as central banks struggle with the availability of fewer levers at their disposal.

Ms. Sara Potter is a Senior Content Specialist and Economic Contributor at FactSet. In this role, she develops a wide range of marketing content, as well as curates and contributes to the FactSet Insight blog, providing commentary on a wide range of economic and market topics. Since joining FactSet in 1999, she has led application and content development teams, focusing on the development of products to facilitate the analysis of global markets at a macro level. Prior, she held research economist positions at Toyota and Standard & Poor’s/DRI (now IHS Markit). She earned an M.A. in International Economics and Finance from Brandeis University and a B.A. in Math/Economics and French from Dartmouth College. She is a CFA charterholder.

Consumer Price Index (CPI) for June 2026 is Projected to Rise 3.8% Year-Over-Year

Explore FactSet's June 2025 CPI forecast, estimating a 3.8% rise. Get insights into inflation trends and economic impact for...

Total Nonfarm Payrolls for June 2026 Are Projected to Rise By 100,000

Stay updated with our monthly series analyzing nonfarm payroll data and job trends. Get expert insights and projections to...

Consumer Price Index (CPI) for May 2026 is Projected to Rise 4.2% Year-Over-Year

Explore FactSet's May 2026 CPI forecast, estimating a 4.2% increase. Get insights into inflation trends and economic impact for...

Total Nonfarm Payrolls for May 2026 Are Projected to Rise By 105,000

Stay updated with our monthly series analyzing nonfarm payroll data and job trends. Get expert insights and projections to...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.