While the two approaches to performance attribution explain the same excess return, they are conceptually and mathematically different enough that they will frequently produce inconsistent results. Since the point of analyzing from both perspectives isn’t to instantly validate each other, this kind of discrepancy shouldn’t frustrate you. In this post, I will offer some suggestions on how to proceed when you encounter these types of differences. Our most experienced users jump on these results as an opportunity to gain insight. You can too.

To begin, I should review my terminology. Brinson attribution refers to performance attribution based on active weights. There are different variations, but the effects usually include allocation, security selection, currency, and potentially others. In contrast, risk-based performance attribution decomposes excess return to active risk factor exposures. This is also considered a multi-variate attribution.

Each performance attribution approach has important strengths and weaknesses. In particular, the critical shortcoming of Brinson attribution is that it doesn’t prevent you from selecting a report grouping irrelevant to the portfolio construction process. When mistakenly done, the analysis is not meaningful at best and misleading at worst. Risk-based performance attribution is a good complement to Brinson attribution because it doesn’t suffer from this weakness and inconsistent results warn you to rethink your report groupings.

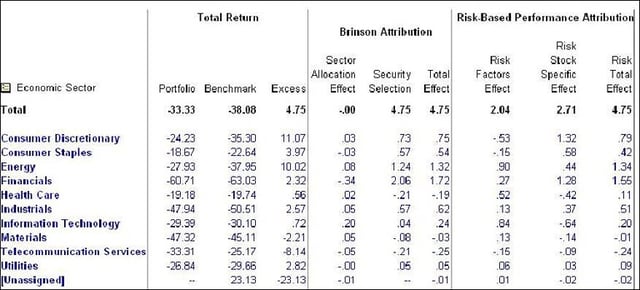

Let's review a sample analysis using a fictitious portfolio to help demonstrate the issue (or opportunity). The analysis below compares performance attribution for the last four quarters using both attribution methodologies simultaneously.

It's clear that the two methodologies differ significantly. The Brinson model attributes the excess return almost entirely to security selection. In contrast, the risk-based performance attribution indicates excess return is attributable to both systematic risk exposures and security-specific decisions. Now what?

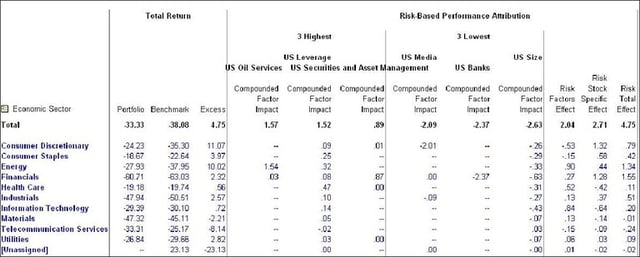

To gain a deeper understanding, first identify what risk factors were the primary sources of (or detractors from) excess return. This is most concisely studied through the following report which reveals size bias as the largest contributor to systematic excess return.

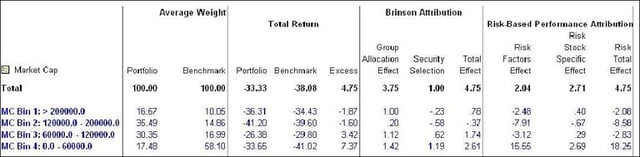

Now, let's use what we learned from our risk-based performance attribution and change the report grouping from sectors to market cap bins.

This change of grouping clarifies how the portfolio was constructed (whether intentional or not). In retrospect, our mistake was the decision to group the report by sector. In this case, the portfolio construction process did not center on sector selection. The conflicting results in the first report warned us to reconsider our analysis.

Risk-based performance attribution has many positive qualities in and of itself. When combined with Brinson attribution, it is a classic case of the whole being greater than the sum of the parts and that means a more complete analysis that leads to more confident conclusions.

Mr. Chris Ellis is Senior Vice President, Head of Strategic Initiatives at FactSet. In this role, he collaborates with our Strategic Business Units on a range of initiatives to help FactSet better address the needs of our clients, most specifically asset managers and asset owners. Mr. Ellis joined FactSet in 1994 in Client Solutions. His career path since then has included successfully defining and expanding the Portfolio Manager Workstation Sales business unit; ultimately, becoming its Vice President before assuming the position of Director of Portfolio Analytics. He subsequently led the development team for FactSet’s core workstation. Prior to his current role, he led the business development function at FactSet through a series of successful acquisitions and strategic partnerships. Mr. Ellis is a graduate of Stanford University and a CFA charterholder.

Total Portfolio Approach: The Plumbing Beneath the Philosophy

Explore this FactSet perspective on the total portfolio approach. Learn factors to consider if you want to effectively...

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.