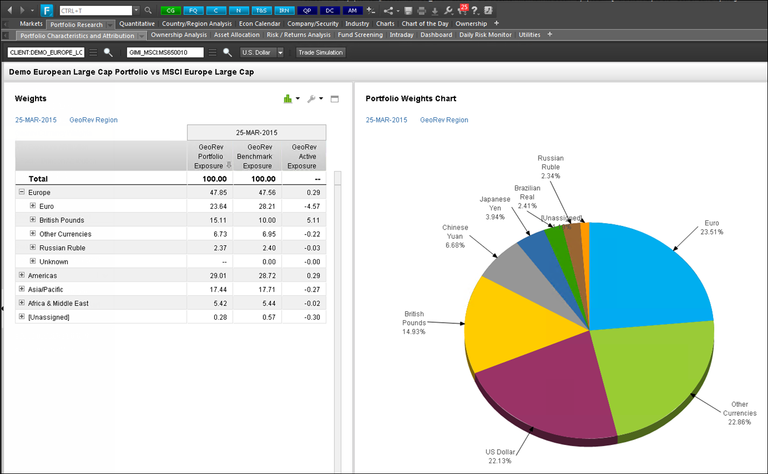

News of the Swiss National Bank unpegging the Swiss Franc from the Euro took the world by surprise earlier this year. Among other side effects, this move from the SNB hurt Swiss companies that rely on sales to other countries in the Eurozone as the cost of Swiss goods and services skyrocketed with the exchange rate. Attention has now turned to other countries with Euro-pegged currencies that might follow suit, with the Danish Krone being of particular concern. We examined a sample European Large Cap portfolio benchmarked against the MSCI Europe Large Cap Index to identify the portfolio’s true exposure to revenues from the Eurozone and evaluate the potential impact of a major currency shock. Using FactSet GeoRev data, we uncovered an exposure of over 20% to the Eurozone, based on the revenue stream of the companies we own. This represents a material portion of our portfolio that is susceptible to changes in revenue coming from the Eurozone.

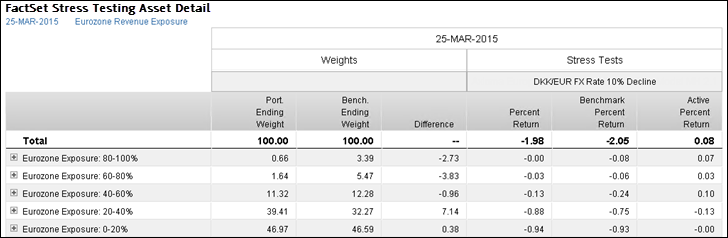

Next we examined securities by levels of exposure to the Eurozone and applied Stress Testing to evaluate the sensitivity of each group to a drastic shift in the DKK/EUR exchange rate.

If the Danish Krone is unpegged from the Euro, and as a result the DKK/EUR exchange rate declines sharply, our portfolio would decline 1.98%. Considering active return, the portfolio actually outperforms by 7 bps relative to the MSCI Europe Large Cap. As one might predict, groups at all levels of exposure take a hit under this scenario. Contrary to expectations, however, our holdings with less revenue exposure to the Eurozone seem to be the most susceptible to negative movement of the exchange rate. Likely driven by our relative underweight, the 20-40% exposure group detracts the most from our active performance. A more striking result may be the highest positive active return contribution of 10 bps from the 40-60% exposure group, given a very small active weight. This result could signal other biases (e.g., sector, industry) influencing performance in this group.

From here we can examine how sector, valuation, or other group bets might be driving the sensitivity to the Eurozone and potential exchange rate movements. With the rise of the dollar also playing a large role in the shape of the European economy, perhaps investigation into USD exchange rate movements could be a next step of analysis.

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

Stress Test Your Portfolio Using 1990 and 2003 Middle East Conflict Scenarios

Explore how to leverage two FactSet hypothetical scenarios based on historical Middle East conflicts and stress test your...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)