Traditionally, bond nerds think of several standard risks: interest rate risk (measured by duration), credit risk (measured by rating or spread), and issuer exposure (typically a concentration measure) to name a few. Investors would not be wrong to summarize their portfolios in this context and happily clip their coupons.

Nevertheless, there are other risks that fixed income investors have to be aware of—I have previously written about liquidity risk and the notion of hidden geopolitical risk. One dataset that seems to be ignored by fixed income investors is Environmental, Social, and Governance (ESG) factors.

Take LQD, the most heavily traded investment grade bond ETF (nearly $8 billion in inflows YTD as of this writing). Investors in LQD would summarize key risks as an effective duration of just over 8.0, an average credit rating of A-/BBB+, and an average spread of ~130 bps over treasury across 1,700 names and ~400 issuers. That is all fine and good.

However, did you know that by investing in LQD, one is potentially exposed to weapons manufacturers, gambling operations, animal testing, poor supply chain labor conditions, and a myriad of governance issues? Why would you willingly subject your clients’ funds (or your own funds) to these controversial and potentially disastrous factors?

Here and in future articles, I will make the argument that managing exposure to ESG factors is a growth opportunity for fixed income asset managers, displays potential for outperformance globally, and is a value-added risk management technique on an ex-post and ex-ante basis.

ESG strategies have grown dramatically in the equity space over the past decade and will continue to increase in importance for fixed income investors. For now, I want to put a definition around ESG for the unaware and build out a case for future growth in this space.

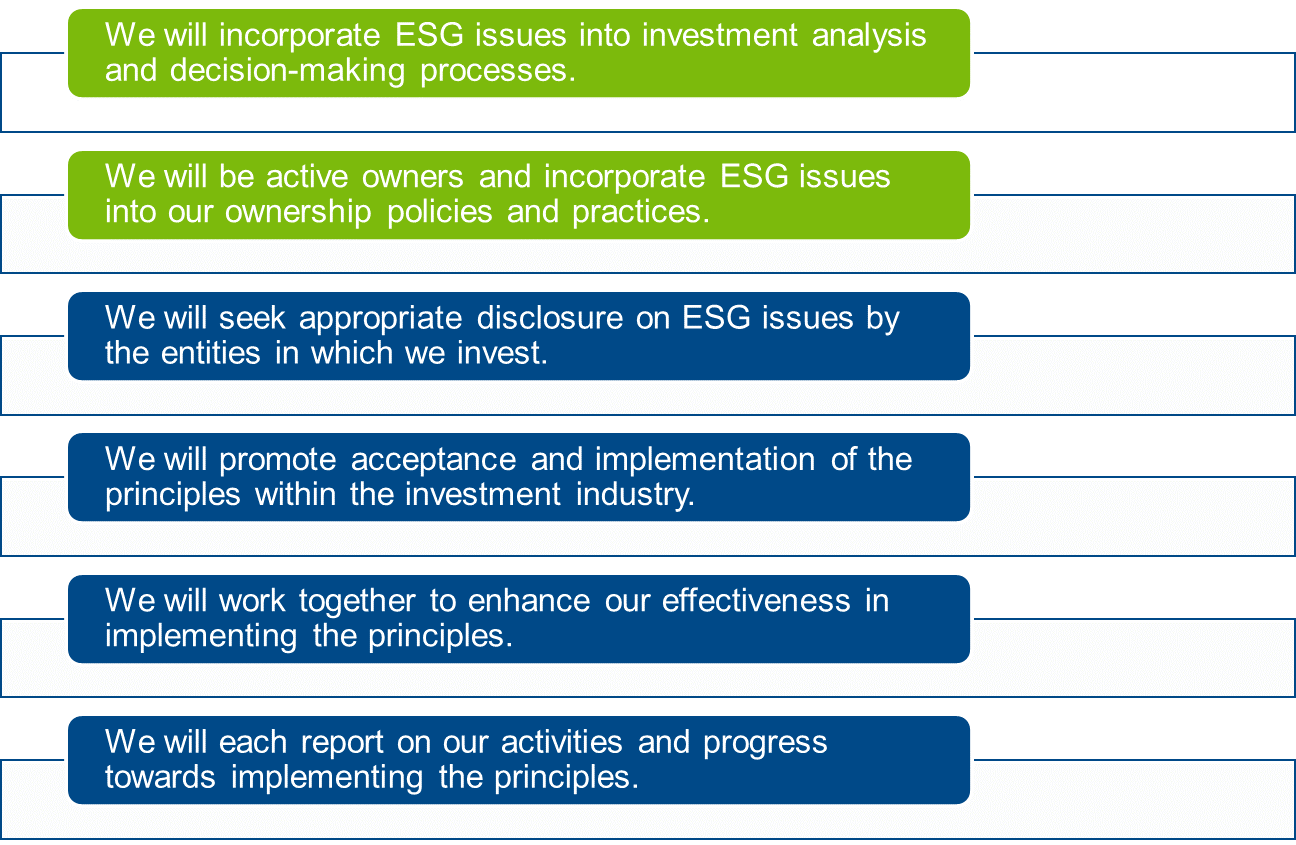

Let’s back up one step. What is ESG? In 2006, the United Nations introduced a mandate called the Principles for Responsible Investing; there are six core components under this umbrella. Participation is voluntary; however, since its launch the number of signatories has grown from 100 to nearly 1,500 managers, representing over $60 trillion in assets under management. A cornerstone of this mandate is the incorporation of ESG factors into the investment decision-making process.

Of the six pillars, I will focus on two. The first is incorporation of ESG issues into an asset manager’s investment analysis and decision-making process. The second is for asset owners as opposed to asset managers: the incorporation of ESG issues into their ownership policies and practices.

The remaining four are the domain of both asset managers and asset owners: encouraging the companies you invest in to voluntarily self-report, promoting the principles across the industry, working across firm/function to enhance the effectiveness of implementation, and remaining open in your reporting and progress on implementation. Like so much in our industry, this tends to be a continual feedback loop.

There are three key reasons why you should you care about ESG principles. First is the growth opportunity for ESG mandates or directives specific to the fixed income space (read: asset gathering). Second is the potential for outperformance. Last, but certainly not least, is improved risk management.

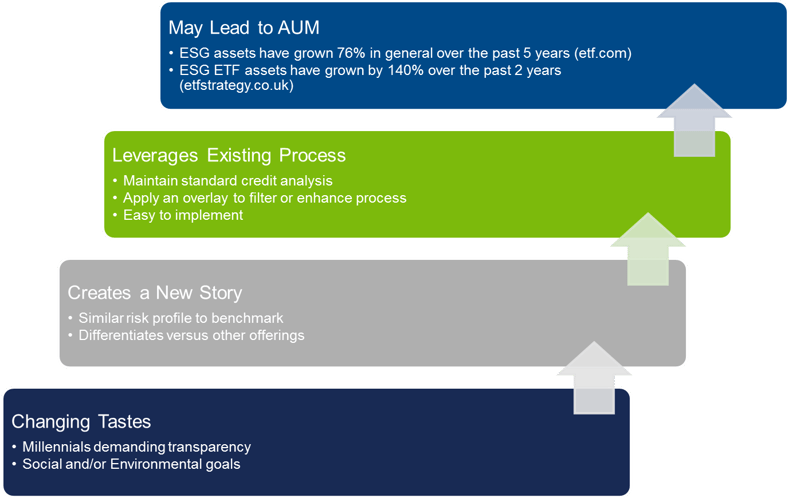

It is not news that the asset management industry is experiencing dramatic change: transition from active to passive, historically low volatility, political regime changes, and millennial investors demanding more transparency to name a few. As we begin the largest wealth transfer in history, they will continue to resonate. In addition, the importance of social and environmental goals and their place in the investment process continues to evolve as clients seek to do good, not just generate Alpha.

A plethora of research highlights show firms with high ESG ratings outperform low-rated or non-rated firms in the equity space; this is not the case in fixed income. However, given a reduction of liquidity and the very real risk that prohibited activities/lack of governance can pose to obtaining the return OF my capital (let alone the return ON my capital), creating awareness of this data is a prudent course of action. In short, the idea is that the Environmental and Social pillars are a morality play; they are the right thing to do, while the Governance pillar is instrumental in ensuring capital preservation.

Incorporating ESG factors also allows managers to tell a new story. It is possible to construct an offering that is similar to a benchmark in terms of duration and spread but without the risk from select activities or poor governance. As interest in passive and smart beta fixed income funds continues to increase, this dataset provides a way to differentiate from other products coming to market.

When reviewing any change or addition to the investment process, understanding the implications is paramount. Incorporating ESG leverages many credit analysis processes. A firm can maintain the same fundamental analysis, review of debt structure, tracking of new issuance, and the resulting feedback loop while overlaying unique content.

The proof is in the pudding. ESG assets have grown 76% annually over the past five years while ESG ETF assets have grown by 140% cumulatively over the past two years. That being said, it remains difficult to find a retail ESG product in the fixed income space. After we explore potential for outperformance and the improvements to risk management, I am confident that this will change.

Check out part two of Pat's ESG in Fixed Income series here: ESG IN FIXED INCOME: ENHANCING RISK MANAGEMENT

Mr. Pat Reilly is Senior Vice President, Senior Director, Mid Office - Americas. In this role, he focuses on providing content, analytics, and attribution solutions to clients across equities, fixed income, and multi-asset class strategies. Prior to this role, Mr. Reilly headed the Fixed Income Analytics team in EMEA and began his career at FactSet managing the Analytics sales for the Western United States and Canada. Before joining FactSet, he was a Credit Manager at Wells Fargo and an Insurance Services Analyst at Pacific Life. Mr. Reilly earned a degree in Finance from the University of Arizona and an MBA from the University of Southern California and is a CFA charterholder.

Total Portfolio Approach: The Plumbing Beneath the Philosophy

Explore this FactSet perspective on the total portfolio approach. Learn factors to consider if you want to effectively...

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.