Active Managers had a rough 2014, with the majority of actively managed funds trailing their respective benchmarks while both the S&P 500 and Dow Jones Industrial Index reached record highs. Much has been made of the strength of the U.S. market relative to the world, but most analysis has only taken into account where a company is domiciled. In this scenario, it is difficult to tell how the strength of the U.S. dollar, which was up 13% in the second half of 2014, impacted the market, since companies are exposed to different currencies while doing business outside of their country of domicile. The question remains, did the strength of the U.S. dollar in 2014 boost companies domiciled in the United States and that do the majority of their business domestically to outperform those domestic companies who did more business internationally?

To perform this analysis we must answer three questions: What do companies do? Who do they work with? Most importantly, where do these companies sell? Historically, geographic revenue data has been difficult to analyze and compare because companies disclose revenue figures subjectively in a non-normalized manner. Solving the geographic puzzle requires a normalized dataset like FactSet GeoRev, which clears a path to analyzing how various market environments, in this case a strong U.S. dollar, affect sales.

To make matters more complicated, U.S. Equity Markets experienced another year of large returns dispersion, highlighted by two of the major domestic indices. The S&P 500 posted a total return range of 1% to 27%, between the 25th and 75th percentiles respectively, with the highest total return of 126% from Southwest Airlines Co. and the lowest return of -60% from Transocean Ltd.

Similarly, the Russell 1000 posted a large return range of -2% to 26% in the same percentile range, with the highest total return of 156% from Skyworks Solutions, Inc. and the lowest return of -77% from Seventy Seven Energy Inc. The S&P 500 and Russell 1000 achieved total returns of 13.7% and 13.2%, respectively, in 2014.

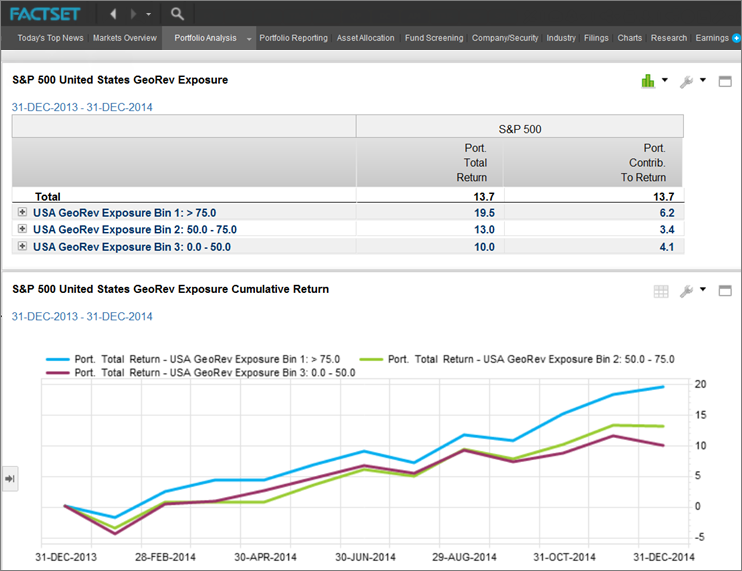

Given the S&P 500 and Russell 1000 returns dispersion in 2014, how can we uncover what was really driving outperformance? Analyzing the GeoRev data of the indices shows us that S&P 500 companies that derived greater than 75% of their revenue from the United States outperformed those who did less than 50% of their business in the same country by a net total return of 9.5%. Could the strength of the U.S. dollar in 2014 account for an outperformance of 19.5% vs. 10.0% for companies that sold mostly within the U.S.?

Simply put, yes. As the strength of the dollar jumped 13% in the second half of 2014, the performance gap widens for the domestic companies that did the majority of their business in the United States versus those that did not.

When valuing companies in a global economy, it has become imperative that we pay close attention to global currency shifts and macroeconomic events—even when doing single country market analysis. Evaluating a company in one geographic dimension is no longer plausible, especially given a market with such disperse return outcomes. Having a normalized GeoRev dataset can help managers exploit global economic and currency trends to pick winners that will add to excess returns. In 2015, that may mean capturing the Euro rebound.

Total Portfolio Approach: The Plumbing Beneath the Philosophy

Explore this FactSet perspective on the total portfolio approach. Learn factors to consider if you want to effectively...

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Insight/Author%20Bios/BadgeNLWF.svg)