If debt provides a large tax advantage, why don’t firms use debt more intensively? Researchers have tried to estimate the benefit of leverage (debt to asset ratio) in several ways. Miller4 starts from the net tax benefit of one dollar of debt versus equity, and then perpetuates the debt to find out its capitalized benefit. On the other hand, Graham3 estimates a tax benefit function by simulating the marginal tax benefit given a firm’s interest deductions.

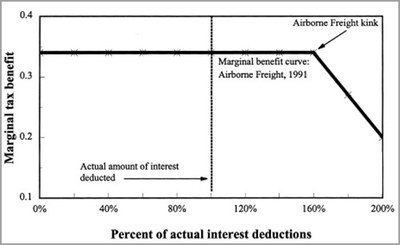

The figure above (Graham3) shows Airborne Freight at the dashed line and that it can increase its leverage ratio so that the interest rate deductions are at 60%. This is where the marginal tax rate benefit function begins decreasing. Graham calculates that increasing leverage can actually add 15.7% to the firm value.

So why don’t firms use a higher leverage ratio? Andrade and Kaplan1 provided a possible explanation in a study of distressed firms. They concluded that financial distress costs equal between 10% to 23% of a firm’s value, and the current debt policy is justified if increasing the leverage ratio increases the probability of distress by 33% to 75%. Comparing these findings with Graham’s results above highlights that even extreme estimates of distress costs do not justify observed debt policies. Firms seem to be over-conservative in using debt and are very under-levered.

To explain this phenomenon, I followed an alternative approach and considered the ex-ante costs of financial distress by estimating the effect of an increase in a firm’s leverage ratio on the decrease in a firm’s credit rating. I used the appropriate econometric modeling to control for the endogeneity of the leverage ratio. (Endogeneity is the main problem of leverage; the same firm-specific variables that are used in rating estimations are also used in leverage estimations).

This model is estimated in two stages: the first stage is the endogeneity control, where leverage is instrumented, and the second stage is where the controlled leverage is used in rating estimation. The table below shows the results:

The first column shows the estimation results for a regular, single stage rating estimation (ordered-probit model) and the second column shows the results for two-stage estimation (IV-ordered-probit model). In the first column, a firm’s profitability (operating income over total assets) has the greatest coefficient. However, in the second column, firm’s leverage has the greatest coefficient. The estimated coefficient of the leverage in the second column is five times the leverage coefficient estimated in the first model.

We can conclude that the leverage coefficient is negatively biased in single-stage estimation, where endogeneity is uncontrolled, and that the endogeneity issue masks leverage. Controlling for endogeneity issue brings out the real impact of leverage on firms’ rating.

To illustrate, let’s look at Goodyear Tire & Rubber Co. 2006 from the FactSet Fundamentals database and try to estimate a possible rating change in 2007. The table below shows the data scaled by coefficient estimates for the single and two-stage models. TheΔRating column shows the cumulative value and the Pr(ΔRating) column converts that value from probit model estimates to probability using the z-table. The single-stage model estimates a 53% probability of increase in the rating, and the two-stage model estimates 66%. In 2007, Goodyear experienced a rating increase to BB- from its prior level B+ in 2006.

As seen in the example above, the largest contribution comes from the change in leverage in the two-stage model. If a firm's leverage has more impact on a firm’s rating change than previously estimated using single-stage models, this may explain why firms shy away from increasing their debt and prefer to stay “under-leveraged.” If the costs of financial distress associated with using more debt increase compared to the tax-shielding benefits of debt, then firms would use debt more conservatively. This may be a partial explanation for the under-leverage puzzle.

1Andrade, Gregor, and Steven N. Kaplan, 1998, How costly is financial (not economic) distress? Evidence from highly leveraged transactions that became distressed, Journal of Finance 53, 1443–1493.

2Ilgaz, Doruk, 2013, What Really Affects a Firm’s Credit Rating? Chapter 2, Doctoral dissertation, Economics Department, University of Houston.

3Graham, John R., 2000, How big are the tax benefits of debt? Journal of Finance 55, 1901–1941.

4Miller, Merton H., 1977, Debt and taxes, Journal of Finance 32, 261–275.

Total Portfolio Approach: The Plumbing Beneath the Philosophy

Explore this FactSet perspective on the total portfolio approach. Learn factors to consider if you want to effectively...

Gold Mining Equity Analysis with the Custom Risk Module

Explore the process to build a bespoke risk model in this FactSet analysis, including data gathering, exposure outlier treatment...

Stress Testing Amid Rising Fears of an AI Bubble

Explore FactSet's stress testing strategies for risk managers amid AI bubble concerns, comparing current market sell-offs to the...

Stress Testing Investment Strategies: Combining Historical Data and Projected Assumptions (Podcast)

Explore portfolio stress testing to assess risk, including appropriate shock factors, historical scenarios and data, and your own...

The information contained in this article is not investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.